Greetings!

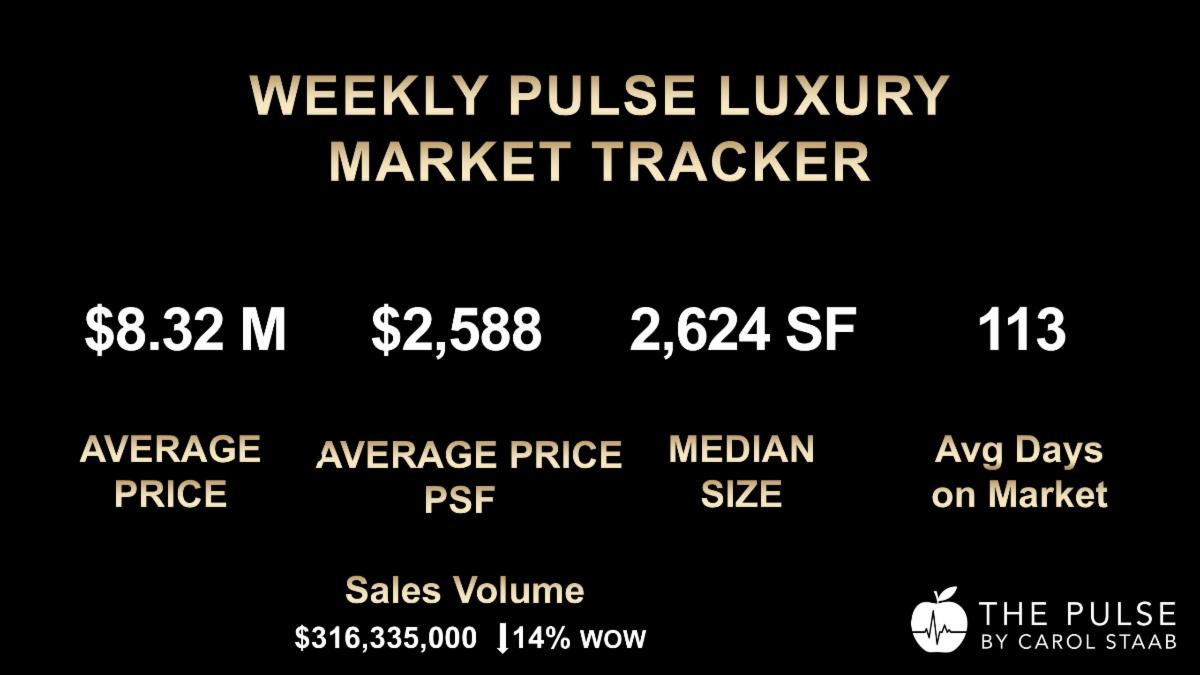

The Manhattan luxury market is not quietly easing into summer. For the second consecutive week, 38 contracts were signed at $4 million and over — nearly double the benchmark of 20 contracts that signals a healthy luxury market. That is not seasonal softness. That is sustained demand. Even more important: this strength is occurring as new inventory begins to tighten. Only 46 new listings came on the market last week, down 26% from the prior week. As we move closer to the slower summer season, we may begin to see new supply dwindle, making well-priced, well-presented inventory even more important. The market is active. But it is not forgiving. Fresh, correctly priced properties are moving. Stale, overpriced listings are still sitting. That is the distinction sellers need to understand . Market Snapshot: Manhattan $4M+ Luxury Market

• 39 contracts signed | up 3 % the prior week • 46 new listings | Down 26% from the prior week • 18 listings went off market | Down 45% from 35 the prior week • $316,335,000 in sales volume | Down 14% from $367,045,000 the prior week • 8 contracts at $10M and over | 21% of luxury activity • 6 new-development contracts | 16% of luxury activity

The decline in weekly sales volume was not a sign of weakness. It reflected the absence of an extraordinary $85 million contract like the one that lifted volume the prior week.

The underlying activity remains very strong.

30-Day Market View

Over the last 30 days: • 159 contracts signed | Down 7% from 171 during the same period last year • 251 new listings | Up 1% from 245 last year • 118 listings went off market | Down 28% from 166 last year This tells a more nuanced story. Contract activity is slightly below last year’s pace, but still strong. New listings are essentially flat. Off-market activity is down sharply, suggesting fewer sellers are pulling back — and more are staying engaged with the market. That matters. When sellers remain in the market and buyers remain active, price discovery improves. The listings that adjust to reality can move.

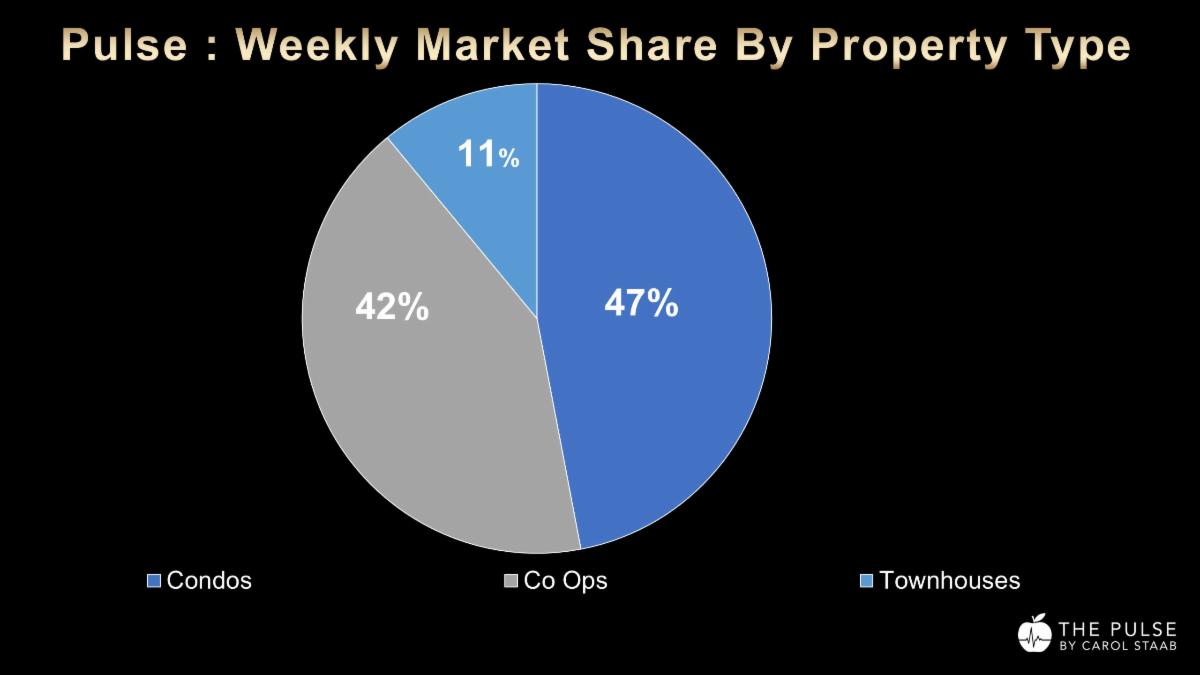

Property Type Breakdown

• Condos: 19 contracts | 47% market share • Co-ops: 16 contracts | 42% market share • Townhouses: 4 contracts | 11% market share

The standout this week was the co-op market. Sixteen co-op contracts at $4 million and over is a very strong showing, particularly in a market where condos often dominate luxury activity. This reinforces an important point: buyers will pursue co-ops when the building, location, scale, pricing, and perceived value are aligned. The co-op market is not weak. Mispriced co-ops are weak.

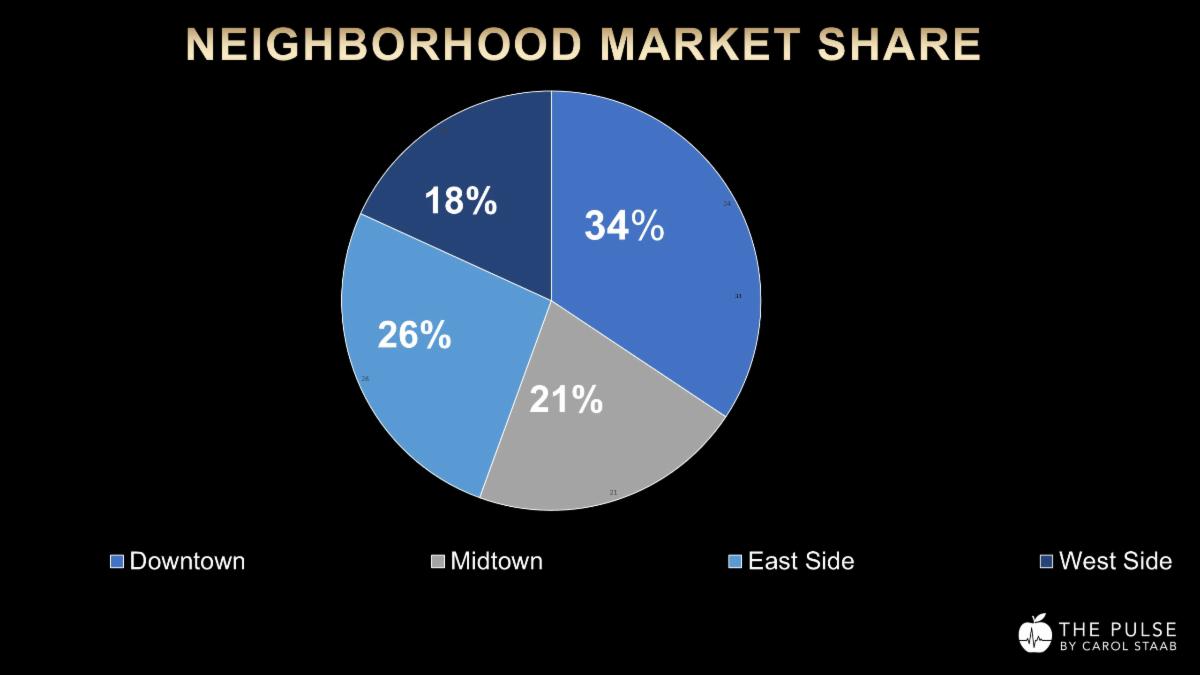

Neighborhood Performance

• Downtown: 14 contracts | 34% market share • Upper East Side: 10 contracts | 26% market share • Midtown: 8 contracts | 21% market share • Upper West Side: 6 contracts | 18% market share

Downtown led the market again, but the Upper East Side had an excellent week with 10 contracts. Midtown also performed well, supported by high-quality condo inventory and continued interest in full-service luxury buildings. The broader message is clear: demand is not limited to one neighborhood. Buyers are moving where they see quality, value, lifestyle, and long-term conviction.

Discounts: Motivated Sellers Are Meeting the Market

Fifteen of the 38 contracts — 39% of the market — received a discount from the original asking price to the last asking price. The median discount was 6.5%.

That is an important signal.

More motivated sellers with stagnant listings are reducing prices to meet the market and secure a deal before the slower summer season. Buyers are active, but they are not indiscriminate. They are negotiating where they see overpricing, long days on market, or a property that has lost momentum. In this market, price reductions are not necessarily a sign of failure. They can be the strategy that unlocks the sale.

$4M+ Market Indicators

$4M+ Market Pulse

The $4M+ Market Pulse registered 4.2, up 0.4 points from last month and up 0.2 points from the same time last year. Definition: The Market Pulse measures the balance between supply and demand. A rising reading indicates that conditions are becoming more favorable to sellers.

$4M+ Climate Index

The $4M+ Climate Index measured 1.70, up 14.9% from last month and up 18.9% from the same time last year. Easy Seller Threshold: 1.25 Challenging Seller Threshold: 0.57

Definition: The Climate Index measures current market conditions relative to seller-favorable and challenging-seller thresholds. Readings above the easy-seller threshold indicate a more favorable environment for sellers.

The $4M+ Climate Index remains comfortably above the easy-seller threshold. That does not mean every seller is in control. It means the market environment is favorable for sellers who are priced and positioned correctly.

$10M+ Market Indicators

The $10 million and over market had another strong week, with 8 contracts signed, representing 21% of all $4M+ luxury activity.

$10M+ Market Pulse

The $10M+ Market Pulse registered 3.5, down 1.2 points from last month but up 0.6 points from the same time last year.

$10M+ Climate Index

The $10M+ Climate Index measured 1.31, down 10.3% from last month but up 48.9% from the same time last year. Easy Seller Threshold: 0.86 Challenging Seller Threshold: 0.37 The ultra-luxury market remains well above the easy-seller threshold. Even with a month-over-month pullback, the year-over-year improvement is meaningful. Capital is still moving into Manhattan luxury real estate when buyers see scarcity, quality, and long-term value.

1. The High Line, 500 West 18th Street, PH35B | Chelsea

Asking Price: $26,600,000 New Development 4 Bedrooms | 4.5 Baths 5,059 SF | $5,257 PSF 51 Days on Market

2. 730 Park Avenue, 10/11C | Upper East Side

Asking Price: $26,000,000 Premium Prewar Co-op Duplex 7 Bedrooms | 8.5 Baths Reduced $1.2 million approximately three months ago

Boots on the Ground: What I’m Seeing

Activity in the luxury sector remains very strong. Despite renewed discussion around the pied-à-terre tax, the Manhattan luxury market appears to be operating as usual. Serious buyers are still transacting. Sellers who are realistic are getting deals done. The market is focused less on headlines and more on quality, scarcity, value, and timing.

On the macro level, markets responded positively after President Trump announced a framework deal with Iran. Oil prices dropped, and equities rallied. That matters because oil, inflation, interest rates, and financial-market confidence all influence the psychology of Manhattan luxury buyers.

At the same time, the Federal Reserve is still navigating sticky inflation. With inflation still above the Fed’s 2% target, the consensus is that rates are likely to remain steady for now, with no immediate rate cuts expected.

Manhattan rents are also at record highs. That is important because rent pressure can support the ownership argument, particularly for buyers who are paying premium rents and evaluating long-term housing costs.

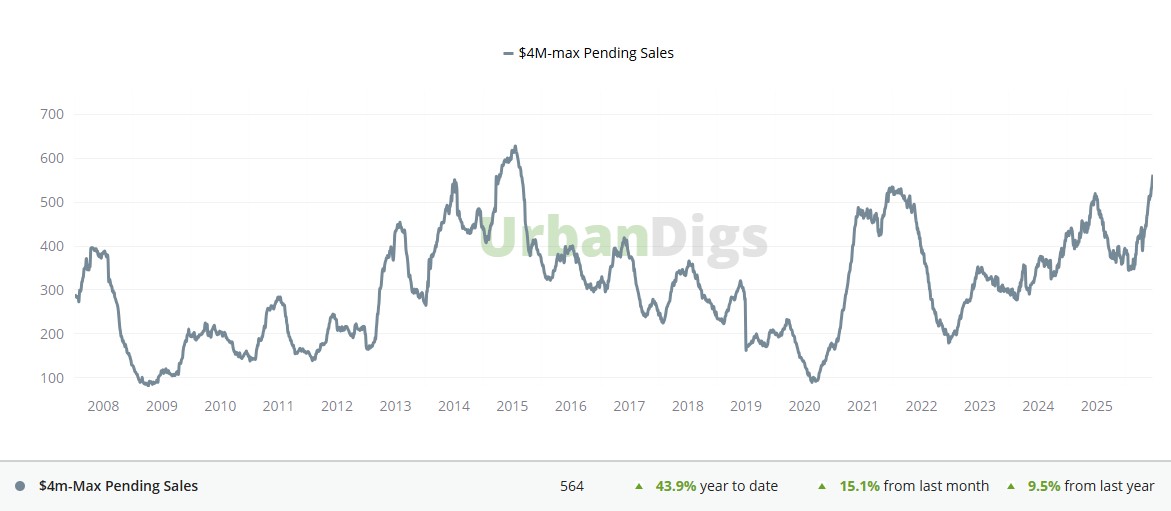

Pending sales are the strongest since the record year of 2022. 554 contracts were signed in the $4M and over market up 43.9% year to date, up 15.1% from last month and up 9.5% from last year. This is a strong signal pointing to a possible price recovery after a decade of relatively flat pricing . See the chart in the boxes below.

It is too early to make that prediction. But market conditions feel more constructive than they have in some time. The current environment has echoes of the period around 2012, before Manhattan experienced a powerful run in sales activity and pricing.

The second-quarter sales results should give us more clarity. For now, the diagnosis is straightforward: The market is very good. But it is selective.

If a property is not selling in this market, the issue is usually one of three things: Pricing. Product. Presentation. The pricing may be too ambitious. The product may have a challenge: building, condition, layout, location, or monthly charges.

Or the presentation may be failing to create desire — weak photography, mediocre marketing, unclear messaging, or a listing narrative that does not communicate why the property matters. In a strong market, those weaknesses become more visible, not less.

Seller Advice

Sellers should be encouraged by this market, but not overconfident. Thirty-eight contracts two weeks in a row is a powerful signal. The Market Pulse is improving. The Climate Index remains seller-favorable. The $10M+ segment is performing well. Co-ops had an especially strong week. But buyers are disciplined.

They are not chasing every listing. They are moving decisively for properties that are well-priced, well-presented, and strategically positioned. If your property has been sitting, now is the time to diagnose the issue before the deeper summer slowdown begins. A thoughtful price adjustment, stronger visual presentation, sharper narrative, or more targeted marketing strategy can change the outcome.

The market is giving sellers an opportunity. But only the prepared sellers will benefit from it.

Buyer Advice

Buyers should not assume summer will automatically bring weakness. Yes, new inventory may decline in the weeks ahead. But that could make the best listings more competitive, not less. If quality inventory becomes thinner, buyers may have fewer strong choices. The best buyer strategy now is preparation. Know the buildings. Understand the pricing history. Compare carrying costs. Watch for reductions. Pay attention to listings that have been repositioned. And when the right property appears, be ready to move. There is still negotiability, especially for stale inventory. But the strongest opportunities may not be the listings with the largest discounts. They may be the properties where the market has not yet fully recognized the value.

Final Thoughts

The Manhattan luxury market delivered another impressive week. Thirty-eight contracts at $4 million and over — for the second week in a row — confirms that buyer demand remains active as we approach the summer season. The market is not euphoric. It is not broad-based. It is not forgiving. But it is strong.

For sellers, this is a moment to be strategic, not passive. For buyers, it is a moment to be informed, prepared, and decisive. The data tells us what happened. The diagnosis reveals what to do next.

If you are considering selling, evaluating your property’s current market position, or trying to understand how today’s luxury market affects your next move, I would be pleased to share a private, customized perspective.

If you found this edition of The Pulse valuable, please consider sharing it with a friend, colleague, client, or advisor who follows Manhattan luxury real estate.

Warm regards, Carol Carol Staab Ranked by Real Trends -Top 1.5% of real estate professionals nationwide Top 100 Sotheby's Company Wide Global Real Estate Sales Advisor My Notable Sale Ritz Carlton $28.4M Sotheby's International Realty. Email: [email protected] Cell: 917-273-7787 "The Pulse: Where data becomes insight. And insight drives results."Website: CarolStaab.Com Subscribe to the Pulse Here |