The Pulse - Manhattan Luxury Market 03/23/2026

Pulse

Pulse

Manhattan Luxury Market Update: Contracts Surge 27% as Inventory Tightens and Demand Holds Firm

Contract activity rebounded sharply last week, with $4M+ deals rising 27% week-over-week and 6% month-over-month, signaling renewed momentum in Manhattan’s luxury market. While weekly fluctuations are expected, the broader trend remains clear: demand is steady—and increasingly shaped by a tightening supply environment.

Over the past 30 days, 130 contracts were signed, exceeding the 123 recorded during the same period last year, reinforcing a market that continues to absorb well-positioned inventory.

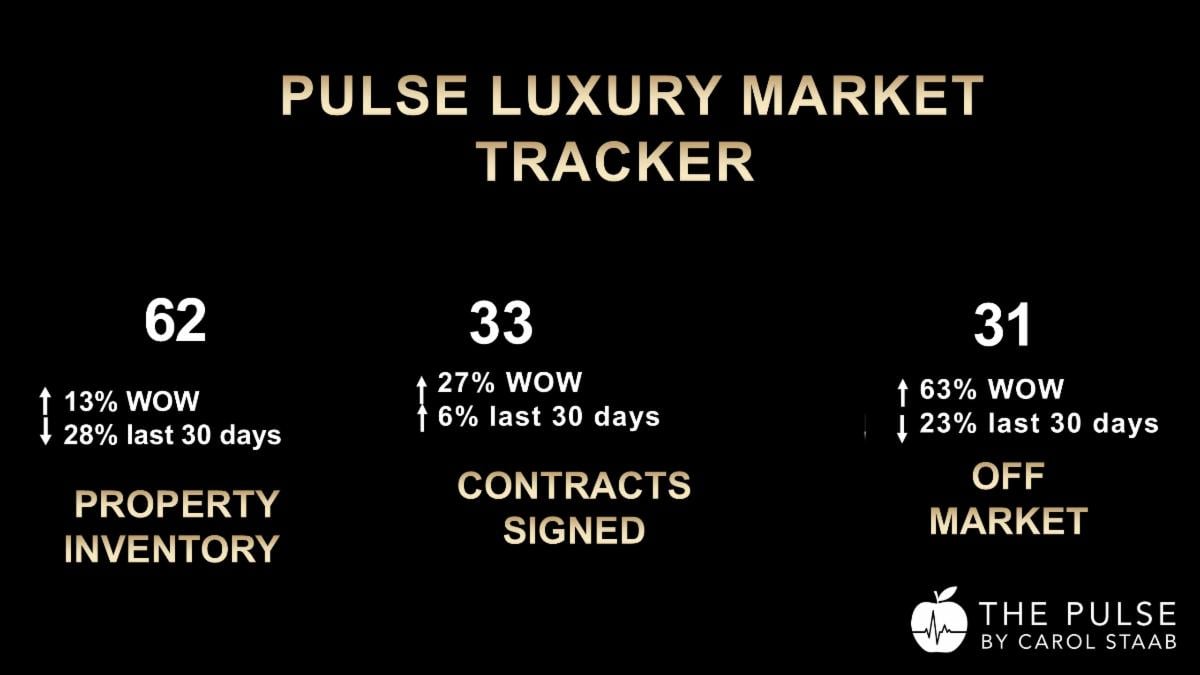

Contracts Signed (Weekly): 33

Prior Week: 26 → Up 27% week-over-week

Contracts Signed (30 Days): 130

Same Period Last Year: 123 → Up 6% year-over-year

New Listings (30 Days): 190

Same Period Last Year: 265 → Down 28% year-over-year

Listings Removed (Weekly): 31

Prior Week: 53 → Down 42% week-over-week

Listings Removed (30 Days): 83

Same Period Last Year: 108 → Down 23% year-over-year

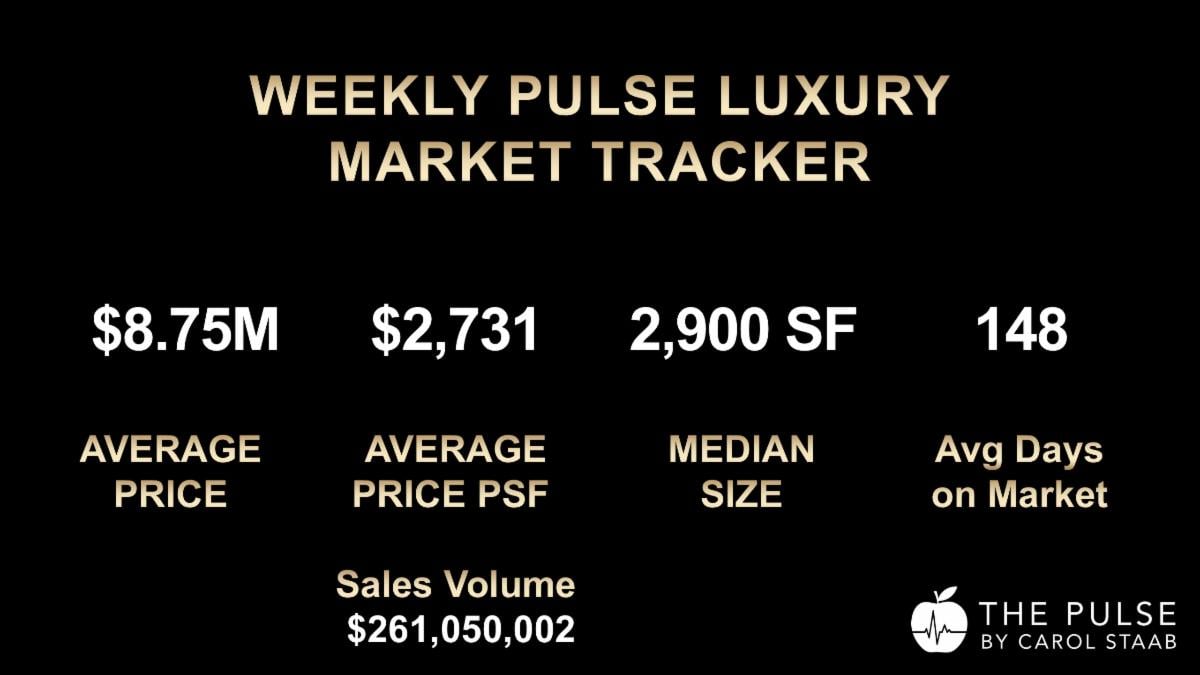

Sales Volume (Weekly): $305,610,000 → Up 17% week-over-week

The takeaway: Inventory is contracting at a meaningful pace, while demand remains consistent—creating a more competitive landscape for well-positioned properties.

Market Pulse: Measures the balance between supply and demand in Manhattan’s luxury market. Higher readings indicate stronger demand relative to available inventory.

Climate Index: Measures the ratio of signed contracts to listings withdrawn without selling, providing insight into how effectively the market is absorbing inventory relative to failed supply.

Market Pulse: 4.2

Climate Index: 1.58

Interpretation: While Market Pulse softened slightly month-over-month, the Climate Index reflects a decisively seller-favorable environment, driven by limited supply and efficient absorption of inventory.

Contracts: 9 (33% market share)

Market Pulse: 5.35

Climate Index: 1.29

Interpretation: The ultra-luxury segment continues to demonstrate depth and resilience, with strong year-over-year gains reinforcing sustained demand at the top of the market.

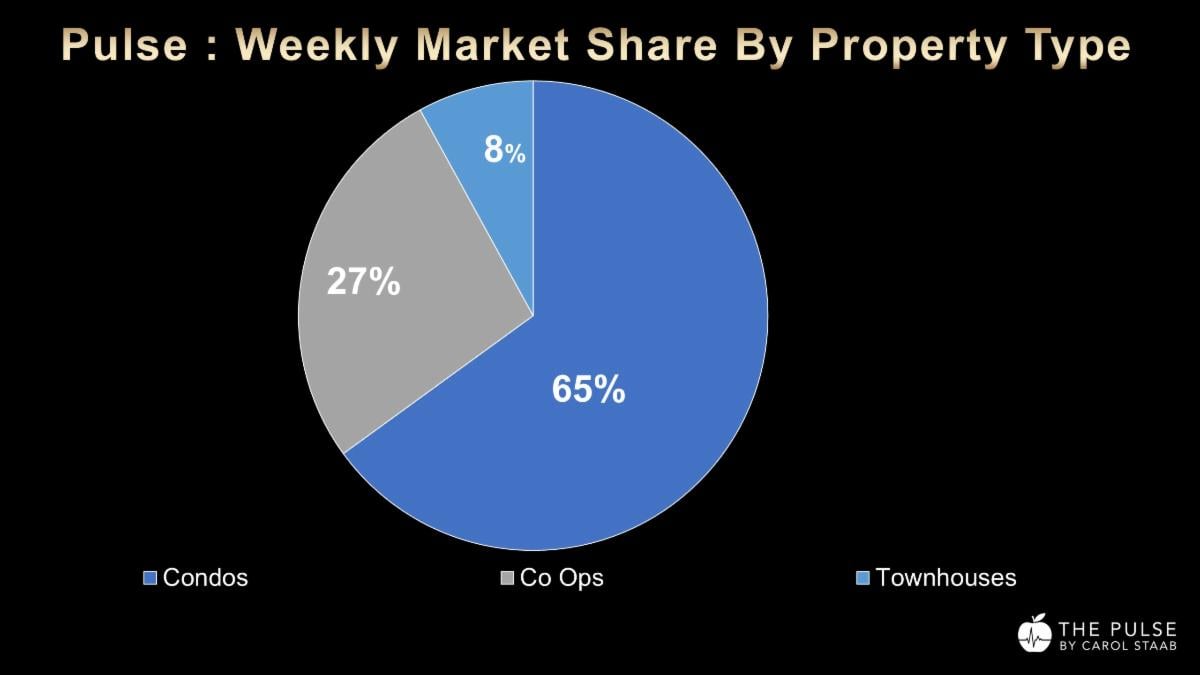

Condominiums continue to dominate transaction activity, reflecting ongoing demand for flexibility, newer product, and turnkey living.

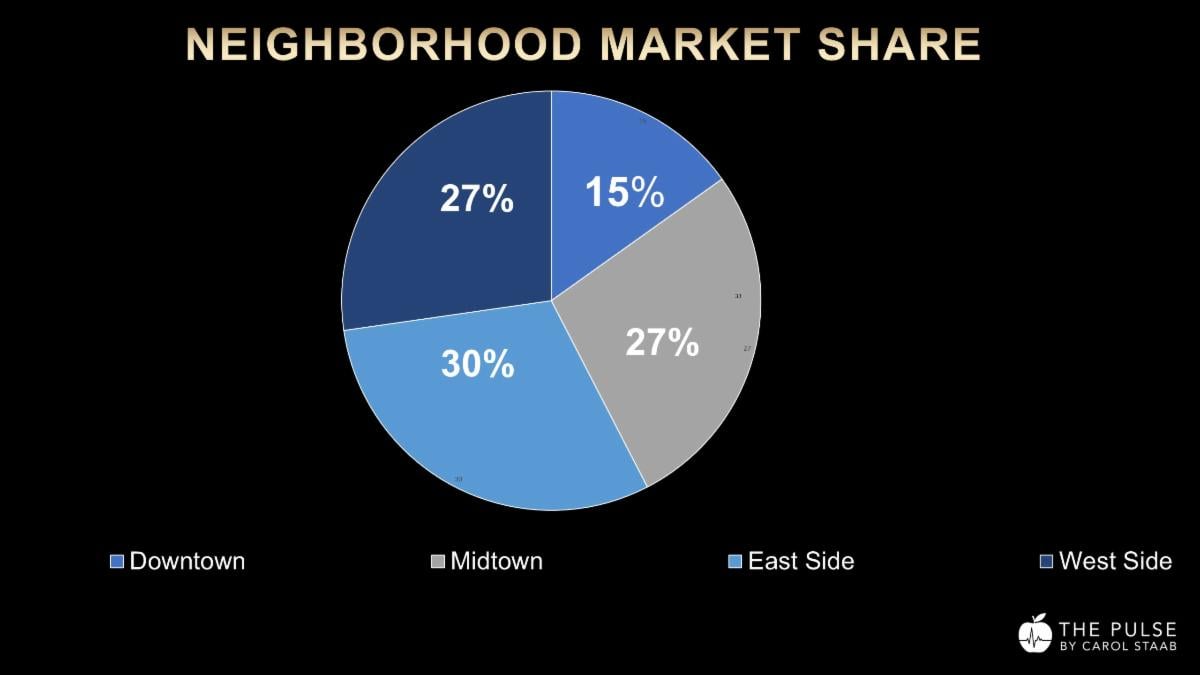

Notably, the Upper East Side led contract activity last week, a departure from the typical pattern where Downtown often dominates luxury transactions.

This shift suggests renewed strength on the Upper East Side, as buyers continue to recognize value across both luxury condominiums and premier prewar co-ops.

Discounting remains relatively contained, indicating that well-priced properties continue to attract serious buyers without significant negotiation pressure.

New development continues to capture a significant share of activity, particularly in higher price points where buyers prioritize turnkey residences and modern amenities.

#1 — 15 East 63rd Street

Upper East Side | Townhouse

Price: $34,500,000

Bedrooms: 7 | Bathrooms: 8.5

Size: 18,000 sq. ft.

Price per Sq. Ft.: $1,916

Days on Market: 426

A notable townhouse transaction that underscores continued demand for scale, privacy, and prime Upper East Side locations, even after extended time on market.

#2 — 200 East 75th Street

Upper East Side | New Development Condo

Price: $19,700,000

Bedrooms: 5 | Bathrooms: 5.5

Size: 4,928 sq. ft.

Price per Sq. Ft.: $3,997

Days on Market: 464

This contract reflects sustained appetite for large-format, luxury new development residences in established Upper East Side corridors.

While condominiums continue to dominate overall contract activity, there are clear signs that buyers are actively pursuing value—particularly in well-located prewar co-ops.

A recent experience illustrates this shift. My listing at 860 Fifth Avenue, a three-bedroom residence with tree-line Central Park views, had not been renovated in over 30 years and was priced at $4.3M. Within days, it generated three all-cash offers above $5.1M—and I continue to receive multiple inquiries each week.

At the same time, I’m seeing the opposite dynamic play out in certain segments of the market. In some cases, sellers are choosing to increase pricing even when strong offers are on the table—often resulting in stalled momentum.

The contrast is telling. In today’s market, buyers are highly responsive to value—and equally quick to disengage when pricing disconnects from reality.

The result is a widening divide:

Strategically priced properties are attracting competition and strong offers

Overreaching pricing is stalling momentum, even in desirable locations

This is a market that rewards precision.

Properties that succeed today are:

In a supply-constrained environment, well-positioned properties have a distinct advantage—often attracting strong interest with limited discounting.

Opportunities still exist—but they require a strategic lens.

The most compelling value is often found in:

In today’s market, success comes from understanding both the data and the nuance behind each opportunity.

Contract activity strengthened last week, but the more important shift is unfolding beneath the surface: inventory is declining while demand remains steady.

This imbalance is creating a more competitive environment—particularly for well-positioned properties in prime locations.

As we move deeper into the spring market, the question is no longer whether buyers are active—it’s whether enough quality inventory will meet that demand.

The Pulse — where data transforms into actionable insights for smart real estate decisions.

Carol Staab has an innovative luxury real estate practice that provides an elite level of concierge service through unparalleled world-class marketing and a hands-on business approach. Her mission is to give her clients an exceptional experience while helping them achieve the best results possible.