The Pulse - Manhattan Luxury Market 03/31/2026

Pulse

Pulse

Contract activity softened last week, with 28 signed contracts above $4M, down 15% from the prior week’s 33 deals. However, context matters: activity remains well above the benchmark of 20 contracts, reinforcing that demand—while fluctuating week to week—continues to operate at a healthy baseline.

With only a few days left in March, a broader lens reveals a more nuanced story. While activity has moderated year-over-year, the underlying dynamics point to a market that is absorbing inventory more efficiently, with serious buyers actively competing for well-positioned properties.

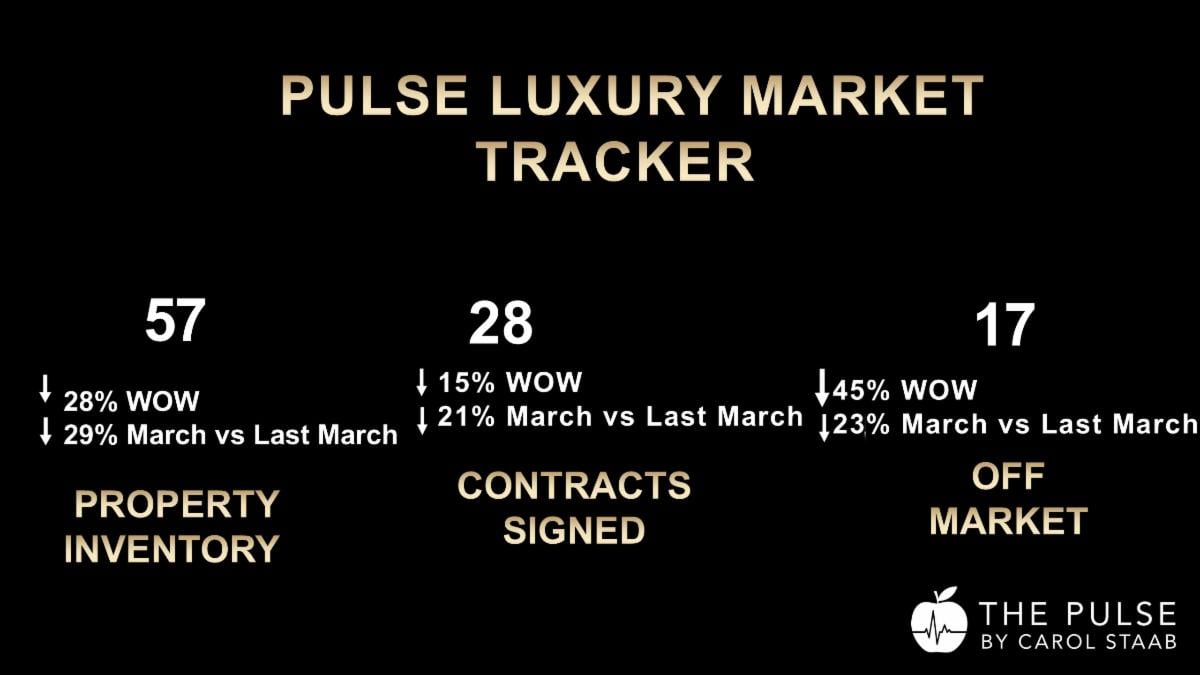

Contracts Signed (Weekly): 28

Prior Week: 33 → Down 15% week-over-week → Still above the 20-contract healthy benchmark

Contracts Signed (March): 126

March 2025: 152→ Down 21% year-over-year

New Listings (Weekly): 57

Prior Week: 62 → Down 8% week-over-week

New Listings (March): 231

March 2025: 327 → Down 28% year-over-year

Listings Removed (Weekly): 17

Prior Week: 31 → Down 45% week-over-week

Listings Removed (March): 87

March 2025: 113 → Down 23% year-over-year

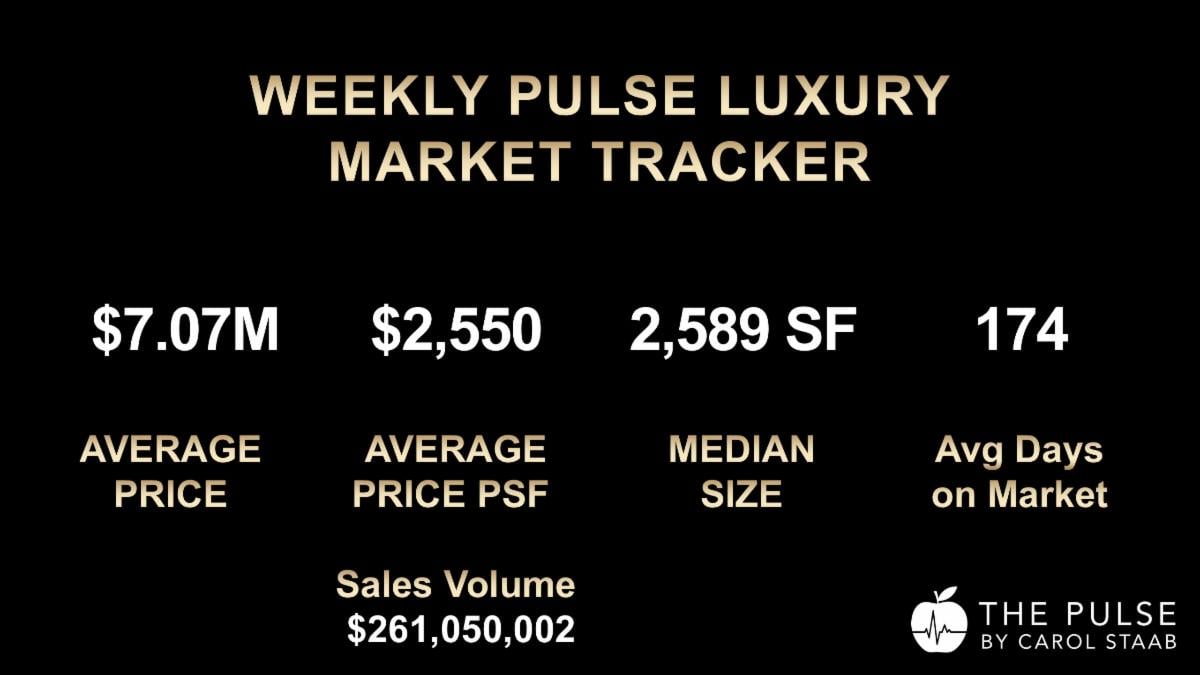

Sales Volume (Weekly): $198,045,000

Prior Week: $261,050,000 → Down 24% week-over-week

Key takeaway: While contract volume has moderated, inventory contraction remains the dominant theme, and sellers are seeing greater success converting listings into deals rather than withdrawals.

Market Pulse measures the balance between supply and demand.

Higher values indicate stronger demand relative to available inventory.

Climate Index measures how efficiently listings are being absorbed by comparing contracts signed to listings removed without selling.

Higher readings indicate a more favorable environment for sellers.

Market Pulse: 3.6

→ Down 1.1 points month-over-month

→ Up 1.5 points year-over-year

Climate Index: 1.58

→ Up 75.6% month-over-month

→ Up 53.4% year-over-year

→ 1.26 = “easy” market threshold

→ 0.57 = “challenging” market threshold

Interpretation: Despite a modest softening in Market Pulse, the Climate Index firmly signals a seller-favorable market, driven by constrained supply and strong absorption.

Contracts: 4 (14% market share)

Market Pulse: 4.3

→ Down 4.1 points month-over-month

→ Up 2.7 points year-over-year

Climate Index: 1.29

→ Up 69.7% month-over-month

→ Up 111.5% year-over-year

→ 0.86 = “easy” market threshold

→ 0.38 = “challenging” market threshold

Interpretation: The ultra-luxury market continues to show depth and resilience, with strong year-over-year improvements in absorption despite week-to-week variability.

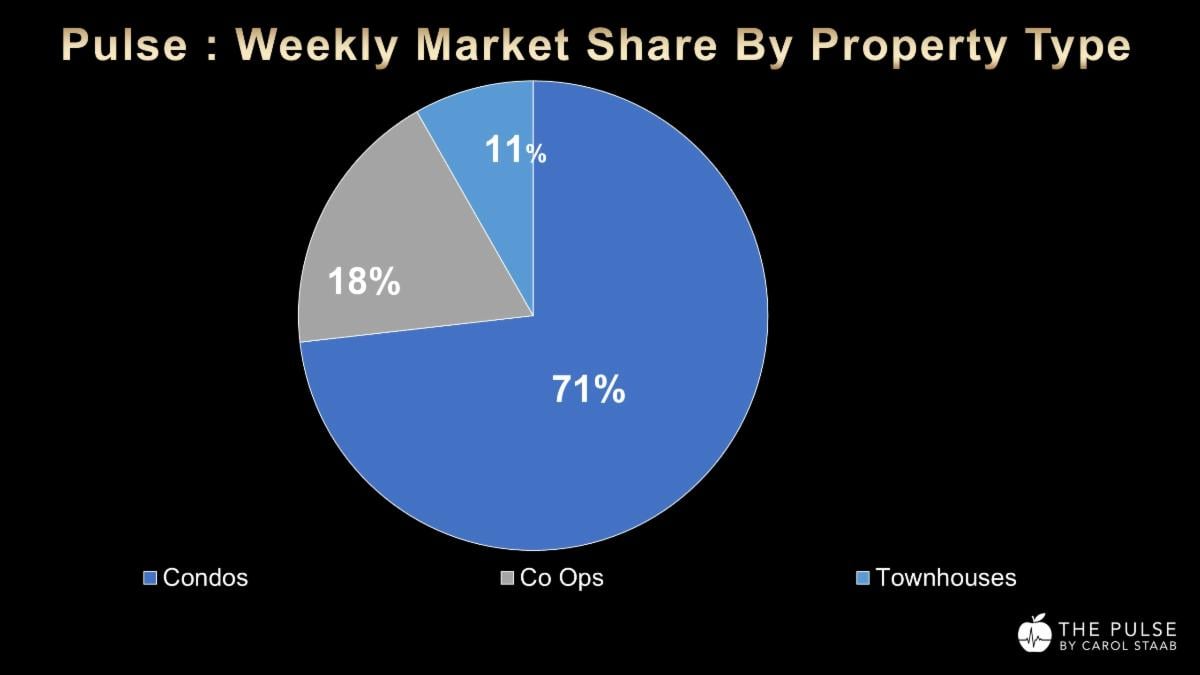

Condominiums continue to dominate, reflecting sustained demand for turnkey living, flexibility, and modern product.

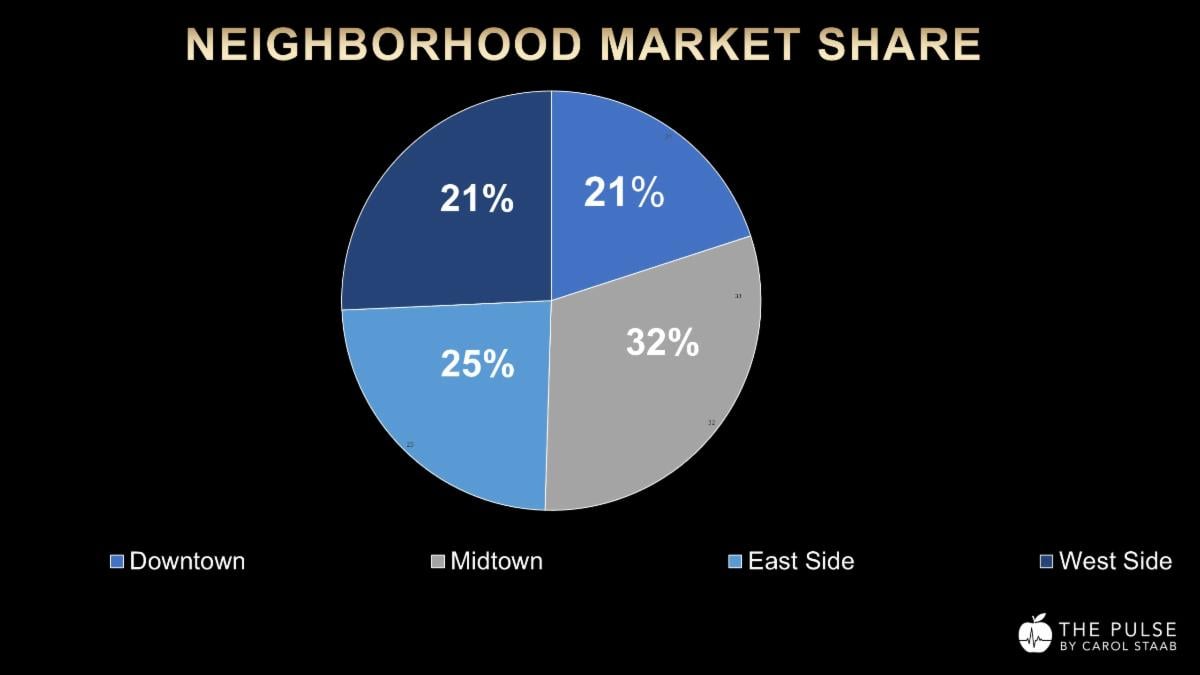

Midtown led activity this week, driven in part by new development and high-end condominium inventory, while the Upper East Side continues to show steady depth across both co-ops and condos.

Discounting remains present but controlled, reinforcing that well-priced properties are trading with discipline—not distress.

New development maintains a meaningful share, particularly in higher price points where buyers prioritize amenities, condition, and immediate usability.

#1 — 15 Central Park West, #8B

Upper West Side | Condo Resale

Asking: $23,000,000

4 Bedrooms | 4.5 Baths

3,478 sq. ft.

$6,612 per sq. ft.

205 Days on Market

Nearly two decades after launch, 15 CPW continues to deliver exceptional resale performance, underscoring the enduring value of premier product and location.

#2 — 1049 Fifth Avenue, #19B

Upper East Side | Condo Resale

Asking: $13,500,000

3 Bedrooms | 3.5 Baths

2,793 sq. ft.

$4,833 per sq. ft.

685 Days on Market

A powerful example of today’s market dynamics: even properties with extended days on market can transact when the right buyer recognizes value.

Wall Street continues to play a critical role in Manhattan’s luxury market:

With Wall Street accounting for 20% of NYC wages while representing just 4% of jobs, the impact on luxury real estate is profound.

I am seeing this firsthand:

The message is clear: capital is active, selective, and ready to deploy.

This is a market that rewards precision and strategy.

To succeed:

With inventory constrained and demand intact, well-positioned properties are achieving results—even in a shifting market.

Opportunities remain—but require a disciplined, informed approach.

Focus on:

In this market, insight—not speed alone—creates advantage.

While contract activity dipped week-over-week, the broader story is far more compelling:

The result is a market defined not by volume alone—but by efficiency, selectivity, and strategic execution.

For properties that haven't reached their full potential - or for sellers preparing to enter the market - strategic positioning is everything! I offer a bespoke analysis to help you maximize value and timing in today's evolving landscape.

Carol Staab has an innovative luxury real estate practice that provides an elite level of concierge service through unparalleled world-class marketing and a hands-on business approach. Her mission is to give her clients an exceptional experience while helping them achieve the best results possible.