|

Greetings!

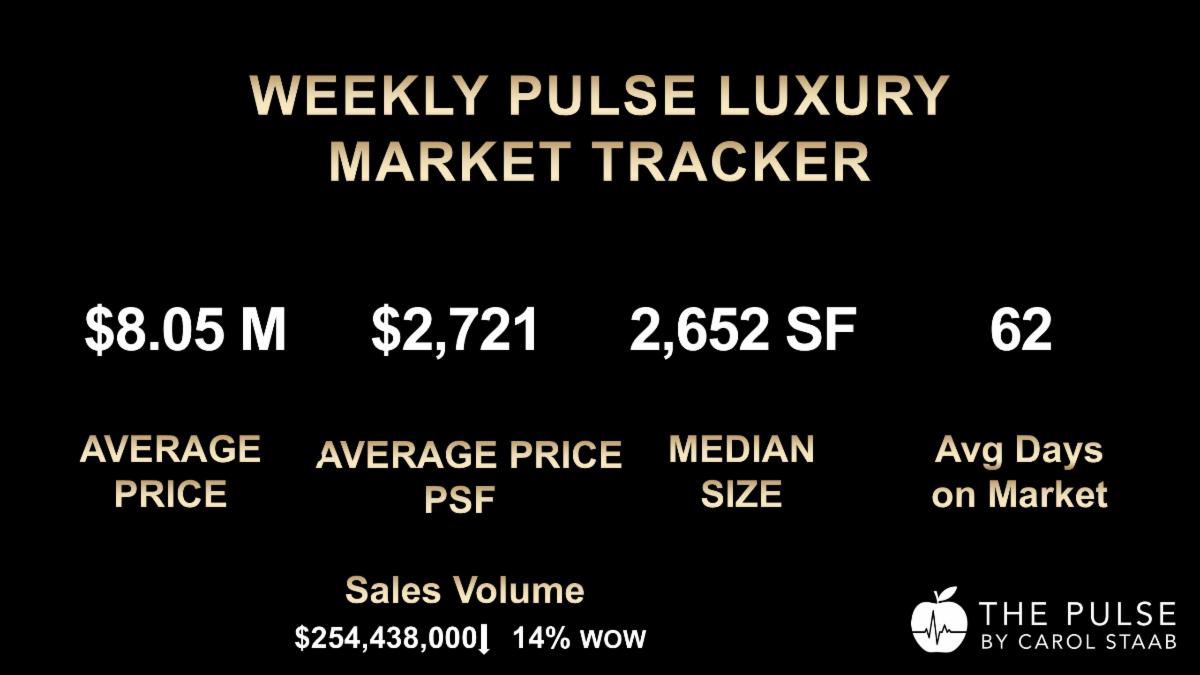

The Manhattan $4M and over luxury market delivered another excellent week, with 33 contracts signed — 1.65 times the 20-contract benchmark typically associated with a healthy luxury market.

Yes, activity was down 10% from last week’s 37 contracts. But context matters.

A 33-contract week is still a very strong result, especially as we move closer to the seasonal point when the Manhattan luxury market often begins to moderate. Even more notable: the $10M and over segment recorded 8 contracts, representing 24% of the market — an excellent showing and a sign that serious buyers are still acting when the property, pricing, and perceived value align.

The message this week is clear: the market remains active, but it is also selective. New inventory is still arriving, fewer properties were pulled off the market this week, and buyers are responding to listings that feel strategically priced, well presented, and worth moving on.

In Manhattan luxury real estate, momentum is not enough.

The property still has to earn the buyer’s attention.

This is where my Real Estate Doctor approach becomes especially relevant: the data tells us what is happening, but the diagnosis reveals why certain properties create urgency while others sit.

Market Snapshot: $4M+ Manhattan Luxury

The $4M and over market recorded 33 contracts signed last week, down 10% from 37 contracts the prior week.

New listings totaled 54, down 12% from 61 the prior week.

Listings going off market fell sharply to 22, compared with 56 the prior week — a 61% decrease.

That decline in off-market activity is meaningful. Last week, the sharp rise in listings being pulled from the market was a warning sign that not every property was connecting with buyers. This week’s drop suggests less retreat from sellers — but it does not change the larger point: buyers remain selective, and listings still need a clear strategy.

Over the last 30 days:

- 147 contracts signed, down 6% from 156 during the same period last year

- 267 new listings, down 8% from 289 last year

- 139 listings went off market, up 11% from 123 last year

The 30-day picture shows a luxury market that is slightly below last year’s contract pace, with fewer new listings and more listings being withdrawn.

That tells me we are not in a market where everything is simply selling because demand is strong. We are in a market where the right properties are selling.

That distinction matters.

Sales Volume

Weekly sales volume totaled $254,438,000, down 14% from $298,289,999 the prior week.

A lower volume week after a strong prior week is not concerning by itself. What matters more is the quality of the activity — and this week, the depth of the $10M+ market stands out.

With 8 contracts signed above $10M, buyers at the higher end of the market are still participating. They are not absent. They are discerning.

A luxury buyer today is asking a very specific question:

Why this property, why this building, why this price — and why now?

If the answer is compelling, buyers are moving.

Property Type Breakdown

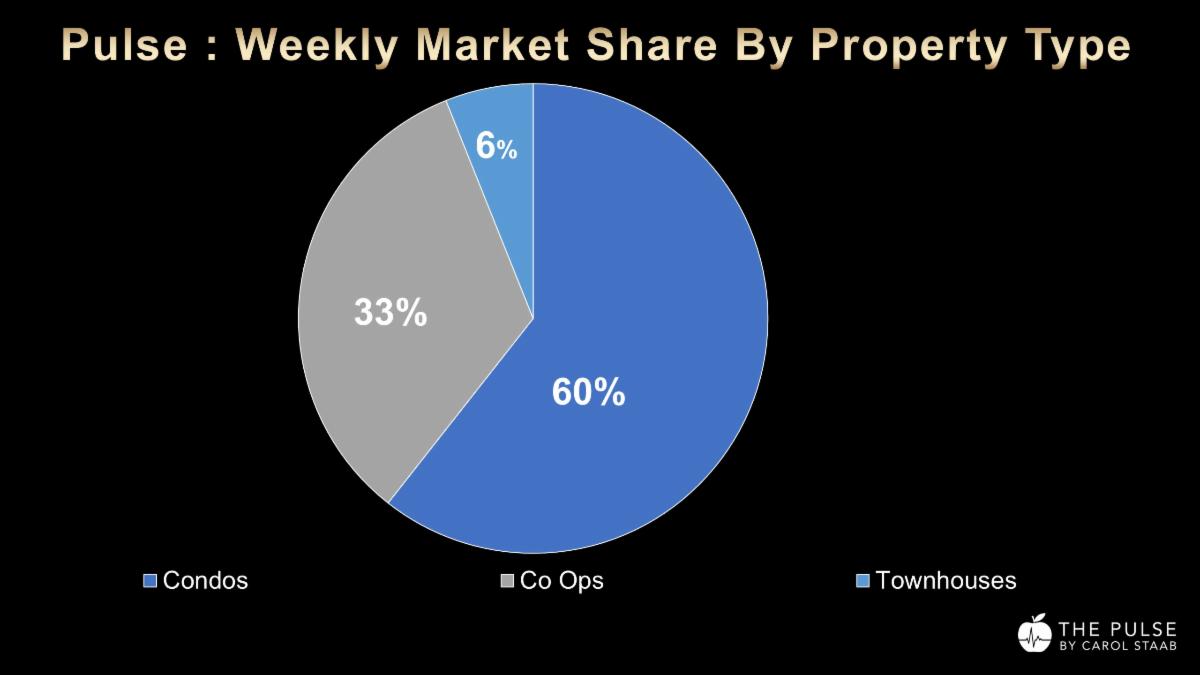

Condos continued to lead the market:

- Condos: 20 contracts | 60% market share

- Co-ops: 11 contracts | 33% market share

- Townhouses: 2 contracts | 6% market share

The condo segment remains the dominant force, which is not surprising given the continued appeal of flexibility, amenities, ease of ownership, and international buyer comfort.

But the co-op activity is also important. With 11 contracts, co-ops represented one-third of the market this week.

That tells me that high-quality co-ops are absolutely still competitive — particularly when they offer scale, architecture, light, views, strong building reputation, and a compelling value proposition relative to condominiums.

In Manhattan, the co-op market is never generic. It is highly specific.

The building matters. The board matters. The financials matter. The story matters.

Neighborhood Performance

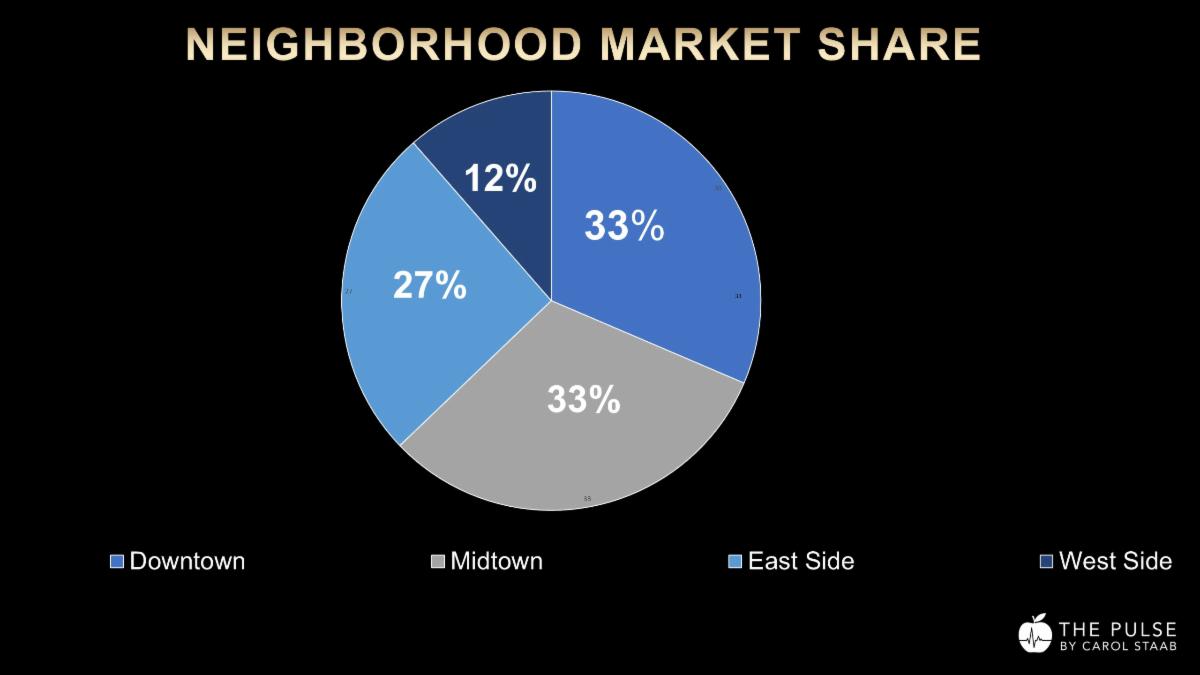

Downtown and Midtown led the week, each with 11 contracts.

- Downtown: 11 contracts | 33% market share

- Midtown: 11 contracts | 33% market share

- Upper East Side: 7 contracts | 21% market share

- Upper West Side: 4 contracts | 12% market share

Downtown continues to attract buyers who want lifestyle, architecture, restaurants, culture, and loft-like living.

Midtown’s strong showing was helped by significant high-end activity, including one of the week’s top contracts at 175 Fifth Avenue.

The Upper East Side remains a steady and important luxury market, particularly for buyers who value prewar architecture, established co-ops, Central Park proximity, full-service buildings, and more traditional Manhattan elegance.

Each neighborhood is performing for different reasons.

That is why broad market reports can miss the nuance. Manhattan is not one luxury market. It is a collection of highly specific submarkets, each with its own psychology, buyer profile, building culture, and value equation.

New Development and $10M+ Market

New development recorded 6 contracts, representing 18% of the market.

That is a healthy share and reinforces that buyers will pay for new product when the offering feels differentiated — design, services, amenities, scale, views, and ease of ownership all matter.

The $10M and over market recorded 8 contracts, representing 24% of all $4M+ activity. That is an excellent performance.

The ultra-luxury buyer is still present, but this buyer is not chasing. This buyer is comparing, waiting, negotiating, and acting only when the opportunity feels justified. The strongest $10M+ listings today are not simply expensive.

They are convincing.

Discounting

There were 12 discounted listings among the signed contracts, representing 36% of the market. The median discount was 8%.

This is an important signal. Buyers are active, but they are still negotiating. They are not blindly accepting aspirational pricing simply because the market is stronger than it was last year.

For sellers, this is where strategy becomes critical.

A price reduction is not a failure when it is part of a disciplined repositioning strategy. But repeated reductions without a new narrative, new visual presentation, or renewed marketing push can weaken perception.

The market does not just respond to price.

It responds to confidence.

Market Indicators

$4M+ Market Pulse

The $4M+ Market Pulse was 3.95, up 0.2 points from last month and up 1.1 points from this time last year.

This indicates a much healthier luxury market than we had a year ago.

The improvement is meaningful because it tells us that the market is not only producing weekly activity — it is operating in a more favorable environment for sellers overall.

$4M+ Climate Index

The $4M+ Climate Index was 1.47, down 24.2% from last month but up 26.7% from this time last year.

For context:

Easy seller threshold: 1.25

Challenging seller threshold: 0.57

At 1.47, the $4M+ market remains above the easy-seller threshold, even though the index has cooled from last month.

That is the nuance.

The market is still favorable for sellers, but it is not a market where sellers can ignore pricing discipline, presentation, or buyer psychology.

$10M+ Market Pulse

The $10M+ Market Pulse was 4.0, down 0.6 points from last month and up 2.1 points from this time last year.

The year-over-year improvement is significant and supports what we are seeing in the contract data: the ultra-luxury market is materially stronger than it was a year ago.

$10M+ Climate Index

The $10M+ Climate Index was 1.46, down 10.6% from last month and up 160.7% from the same time last year.

For context:

Easy seller threshold: 0.87

Challenging seller threshold: 0.38

At 1.46, the $10M+ segment remains well above the easy-seller threshold.

This does not mean every ultra-luxury property will sell.

It means that well-positioned ultra-luxury properties have a far better climate than they did last year — and sellers who understand that distinction have an advantage.

1. 740 Park Avenue, #6/7B

Asking Price: $22,000,000

Property Type: Prewar co-op duplex

Bedrooms: 5

Bathrooms: 5.5

Days on Market: 62

The top contract of the week was a duplex at 740 Park Avenue, one of Manhattan’s most prestigious and storied prewar co-ops.

This contract is a reminder that trophy co-ops remain highly relevant when they offer pedigree, scale, privacy, architecture, and a building name that carries true weight in the Manhattan luxury market.

2. 175 Fifth Avenue, #8 North

Asking Price: $17,625,000

Property Type: New development condo

Neighborhood: Flatiron / Midtown

Bedrooms: 4

Bathrooms: 4.5

Rooms: 9

Size: 3,889 sq. ft.

Price per sq. ft.: $4,532

The second-highest contract was at 175 Fifth Avenue, the Flatiron Building — one of the most iconic buildings in New York.

This contract speaks to the power of architectural identity. In a market where buyers have choices, a property with a clear sense of place and history can stand apart.

New development succeeds when it offers more than new finishes.

It succeeds when it offers a story buyers want to own.

Policy Watch: Proposed Pied-à-Terre Tax and Cash Purchase Surcharge

Two proposed tax measures are worth watching closely because they could affect Manhattan luxury buyer behavior, particularly in the $5M+ segment and among all-cash purchasers.

The first is the proposed pied-à-terre tax on New York properties valued at $5M and over.

One important nuance: the initial assessed value would be based on the Department of Finance valuation, which is often significantly lower than actual market value. As a result, many Manhattan properties may not be immediately affected at the level buyers and sellers might assume.

The proposed Department of Finance rates are:

$1M–$3M: 4%

$3M–$5M: 5.25%

$5M+: 6.50%

After the city develops a new valuation system based on comparable sales, years three through five would use market-value-based rates:

$5M–$15M: 0.80%

$15M–$25M: 1.05%

$25M+: 1.30%

For townhouses, the proposed rates would apply for all five years:

$5M–$15M: 0.80%

$15M–$25M: 1.05%

$25M+: 1.30%

The second proposal is a 1% tax on all-cash purchases over $1M.

This would effectively reduce one of the current advantages of paying cash: avoiding the mortgage recording tax. That matters in New York City, where a large share of purchases are all cash — approximately 60% at the $1M level and, in the $3M+ segment, as many as 9 out of 10 purchases.

My view: this tax proposal package is something to watch carefully.

We saw a similar behavioral pattern before the mansion tax increase. There was a flurry of luxury activity from buyers who wanted to purchase before the increase took effect. Then, after the adjustment, the market largely absorbed it as another cost of buying in New York. That may happen again.

For now, these are proposals, not settled market reality. But uncertainty itself can influence timing. Buyers, sellers, attorneys, accountants, and advisors should be watching closely to see whether these measures move forward — and how they may affect the Manhattan luxury market.

Seller Perspective

Sellers have reason to feel encouraged.

The $4M+ market remains above the easy-seller threshold. The $10M+ segment is meaningfully stronger than it was last year. Thirty-three contracts in one week is an excellent result. And with 8 contracts above $10M, the high end of the market is clearly not dormant.

But the strongest sellers will not interpret this as permission to overprice.

The market is rewarding properties that are well priced, well presented, and clearly positioned. It is not rewarding confusion.

This is the diagnostic work sellers need before they launch — or before they relaunch.

When a luxury property does not sell, the reason is rarely one-dimensional. It may be price, presentation, timing, condition, building perception, buyer targeting, broker outreach, or the absence of a compelling narrative.

My role is to diagnose where the resistance is coming from and reposition the property so the market can see its value more clearly.

That is the difference between marketing and strategy.

- Before launching, a seller should be able to answer:

- Who is the most likely buyer?

- What is the property’s strongest value proposition?

- How does it compare with current competition?

- What objections will buyers have?

- How should the marketing overcome those objections before the showing?

This is where many luxury listings underperform.

They present the facts, but they do not shape the perception.

A listing cannot simply say: beautiful apartment, great building, prime location.

That is not strategy.

Strategy means identifying the buyer, diagnosing the property’s challenges, elevating its strengths, and creating a marketing narrative that makes the value clear.

The best listings do not just go on the market.

They enter the market with intention.

Buyer Perspective

Buyers still have opportunities, but they need to be prepared.

The market is active, the $10M+ segment is stronger, and well-positioned listings can move quickly. At the same time, discounting remains present, with 36% of this week’s contracts reflecting price reductions and a median discount of 8%.

That creates a more nuanced buyer environment.

This is not a market where buyers should assume weakness. It is also not a market where they should feel pressured into poor decisions.

The best buyers will be disciplined and decisive.

Know the building. Understand the board. Study the financials. Compare the property not only by price per square foot, but by light, views, layout, renovation quality, building reputation, monthly charges, resale history, and scarcity.

In Manhattan, value is rarely obvious from the headline price alone.

Sometimes the best opportunity is not the property with the biggest discount.

It is the property where the market has not fully recognized the long-term quality.

Final Thoughts

This was another excellent week for the Manhattan $4M and over market.

33 contracts signed. $254M in sales volume. 8 contracts above $10M.

A $4M+ Climate Index still above the easy-seller threshold.

A $10M+ Climate Index up more than 160% year over year.

The market is not perfect. It is not automatic. And it is not equally strong for every property. But it is active.

For sellers, the opportunity is real — if the pricing, positioning, and marketing are aligned.

For buyers, the opportunity is also real — if they understand the difference between a property that is merely available and a property that is genuinely worth pursuing.

In Manhattan luxury real estate, data tells us what is happening.

Insight tells us what to do next.

If you are thinking about selling this year — or if your property has been on the market without the response you expected — I would be pleased to prepare a private diagnostic review of your property’s positioning, pricing, presentation, and competitive set.

If you found this edition of The Pulse valuable, please share it with a friend, colleague, client, or advisor who follows the Manhattan luxury market.

Warm regards,

Carol

Carol Staab

Top 100 Sotheby's Global Real Estate Sales Advisor

Top 10 for Sotheby's Individuals Manhattan

My Recent Notable Sale Ritz Carlton $28.4M

Sotheby's International Realty.

Email: [email protected]

Cell: 917-273-7787

"The Pulse: Where data becomes insight. And insight drives results."

Website: CarolStaab.Com

Subscribe to the Pulse Here

|