|

Greetings!

The Manhattan $4M and over luxury market delivered a meaningful signal last week: the spring market may not be tapering off as quickly as many expected.

Thirty-eight contracts were signed, up 27% from the prior week. After a somewhat delayed spring season, this increase suggests that buyer activity may be extending beyond the traditional mid-June slowdown and could continue deeper into July.

That matters.

In Manhattan luxury real estate, the market does not always move according to the calendar. Momentum can arrive late, especially when buyers are navigating elevated interest rates, global uncertainty, tighter inventory, and a highly selective landscape.

This week’s data suggests buyers are still very much engaged.

The story to watch now is pending sales.

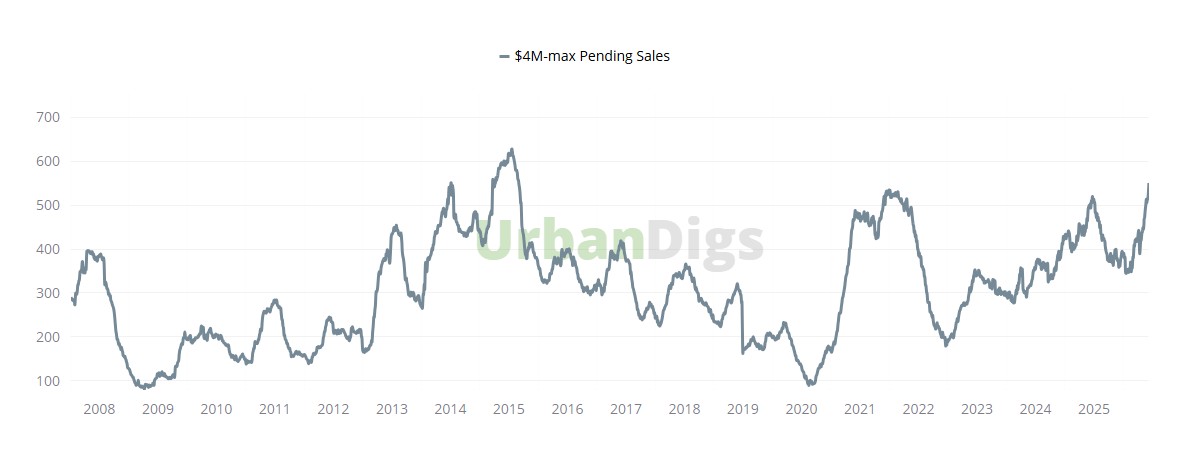

According to UrbanDigs, Manhattan’s residential market and data intelligence firm, $4M+ pending sales reached 552 as of early June. Please see the chart box for reference.

That figure is notable because it exceeds the pending-sales level seen during 2021, one of the strongest contract years in recent memory. The only higher year was 2015.

One week does not make a trend. But the pending-sales data is strong enough to raise an important question:

Is the Manhattan luxury market beginning to emerge from a decade-long period of relatively flat performance?

The data tells us what happened. The diagnosis reveals what to watch next.

Market Snapshot: Manhattan $4M+ Luxury Market

• 38 contracts signed | Up 27% from the prior week

• 62 new listings | Up 22% from the prior week

• 35 listings went off market | Up 16% from the prior week

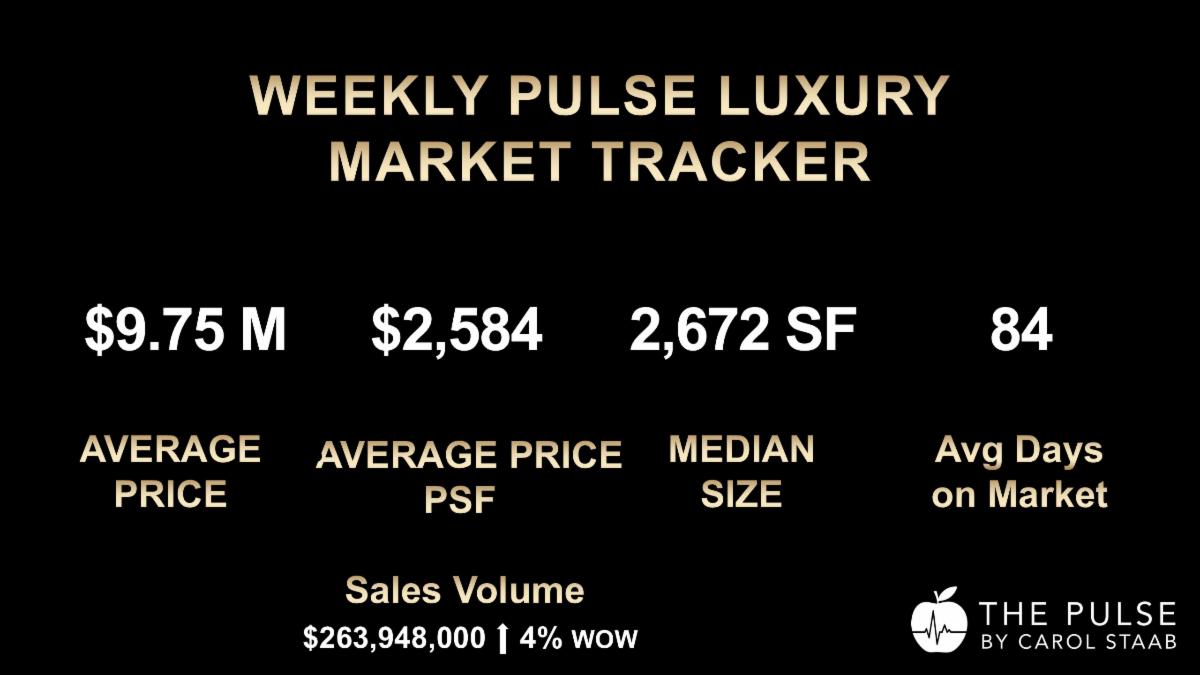

• $367,045,000 in sales volume | Up 39% from $263,948,000 the prior week

• 10 contracts at $10M and over | 26% of luxury activity

May Market Comparison

• 146 contracts signed in May | Down from 158 in May last year

• 238 new listings in May | Down 15% from May last year

• Listings off market in May | Down 13% from May last year

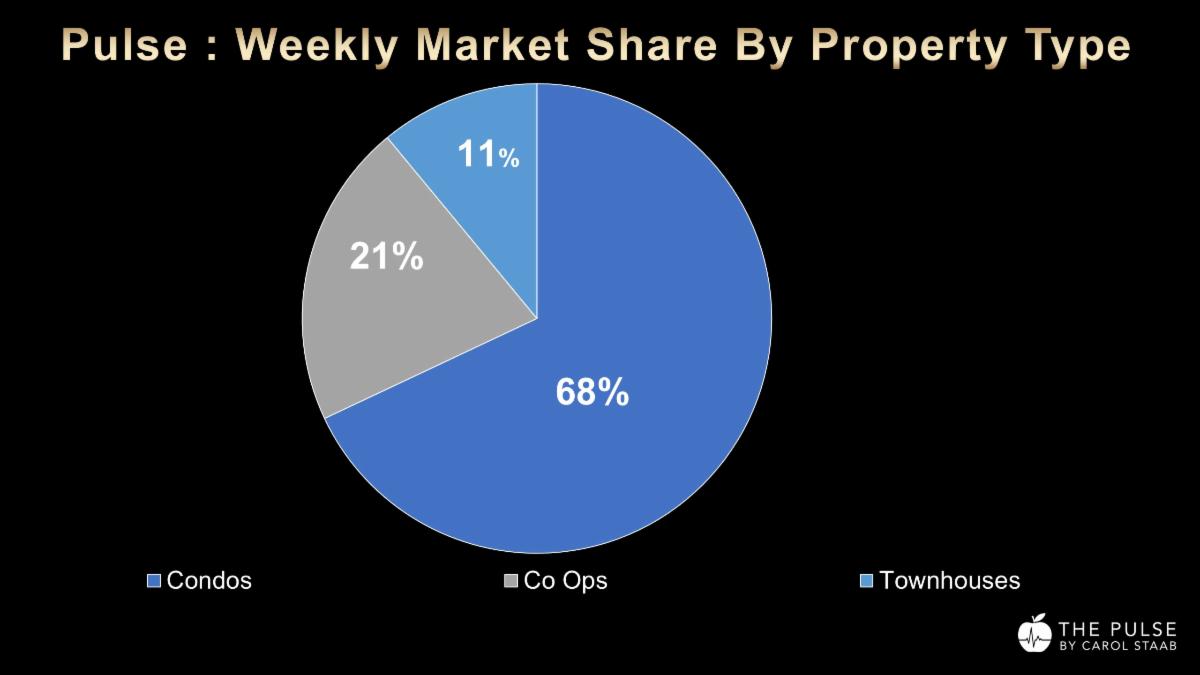

Property Type Breakdown

• Condos: 26 contracts | 68% market share

• Co-ops: 8 contracts | 21% market share

• Townhouses: 4 contracts | 11% market share

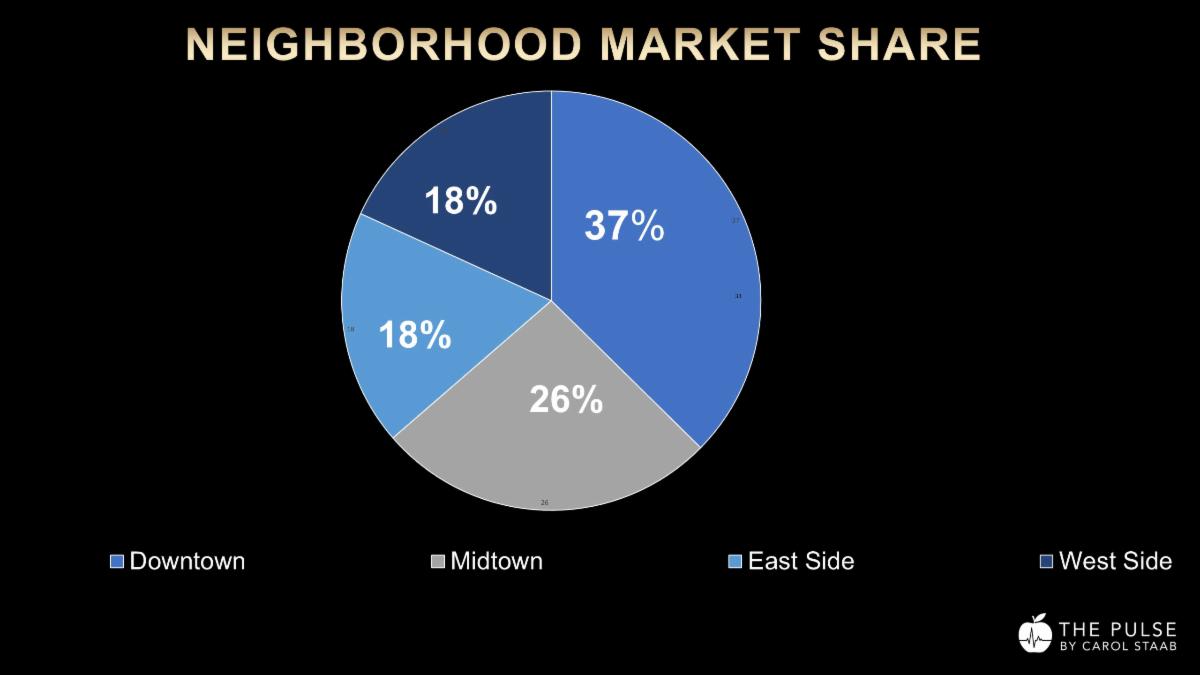

Neighborhood Performance

• Downtown: 14 contracts | 37% market share

• Midtown: 10 contracts | 26% market share

• Upper East Side: 7 contracts | 18% market share

• Upper West Side: 7 contracts | 18% market share

New Development

• 5 new-development contracts | 13% of the market

Much of Manhattan’s luxury new-development inventory has already been absorbed, and there is limited new supply coming through the pipeline. High land costs, construction costs, financing costs, and development economics are making many future projects difficult to justify.

That matters for the broader luxury market.

When new-development supply tightens, buyers who want turnkey, amenitized, high-quality residences have fewer choices. That can push demand toward the best resale properties and increase the value of well-positioned inventory.

This is one reason luxury inventory has become tighter.

Sales Volume

Weekly sales volume rose to $367,045,000, up 39% from $263,948,000 the prior week.

The increase reflects both the rise in contracts and a stronger showing from the ultra-luxury market.

Capital continues to move into Manhattan luxury real estate when buyers see quality, scarcity, and long-term value.

$4M+ Market Indicators

$4M+ Market Pulse

The $4M+ Market Pulse registered 3.85, up 0.2 points from last month and up 0.3 points from the same time last year.

Definition: The Market Pulse measures the balance between supply and demand. A rising reading indicates that conditions are becoming more favorable to sellers.

$4M+ Climate Index

The $4M+ Climate Index measured 1.66, up 12.2% from last month and up 16.1% from the same time last year.

Easy Seller Threshold: 1.25

Challenging Seller Threshold: 0.57

Definition: The Climate Index measures current market conditions relative to seller-favorable and challenging-seller thresholds. Readings above the easy-seller threshold indicate a more favorable environment for sellers.

$10M+ Market Indicators

The $10M and over market had an outstanding week, with 10 contracts signed, representing 26% of all luxury activity.

$10M+ Market Pulse

The $10M+ Market Pulse registered 3.55, down 1.5 points from last month and up 1.1 points from the same time last year.

Definition: The Market Pulse measures the balance between supply and demand. A rising reading indicates that conditions are becoming more favorable to sellers.

$10M+ Climate Index

The $10M+ Climate Index measured 1.31, down 10.3% from last month and up 48.9% from the same time last year.

Easy Seller Threshold: 0.86

Challenging Seller Threshold: 0.38

Definition: The Climate Index measures current market conditions relative to seller-favorable and challenging-seller thresholds. Readings above the easy-seller threshold indicate a more favorable environment for sellers.

1. 48-50 West 69th Street | Upper West Side Townhouse

Asking Price: $85M

5 Bedrooms | 5.5 Baths | 12 Rooms

19,600 SF | $4,336 PSF

Features include a lap pool.

The top contract of the week was the extraordinary townhouse at 48-50 West 69th Street, asking $85 million.

This was the most expensive townhouse contract since the Upper East Side townhouse purchased by Len Blavatnik at 19 East 64th Street.

2. 150 Nassau Street, Skyhouse Penthouse | Seaport Area

Asking Price: $20M

4 Bedrooms | 3.5 Baths | 12 Rooms

6,355 SF | $3,147 PSF

The second-highest contract was the Skyhouse Penthouse at 150 Nassau Street, asking $20 million.

Located near the South Street Seaport, the residence offered substantial scale, dramatic design, and architectural distinction. The property was recognized by Interior Design magazine, including design honors that reinforced its position as a highly distinctive offering.

Insights: What Matters This Week

The most important signal this week is not simply that contracts rose 27%.

It is that the market may be extending rather than fading.

After a delayed spring, stronger contract activity, higher sales volume, and a powerful $10M+ performance suggest that buyer demand remains active later into June than many expected.

Pending sales are the second signal to watch.

With $4M+ pending sales at 552 according to UrbanDigs, the market is showing a deeper level of activity than the weekly contract count alone may reveal. If pending sales continue to hold, this could point to a more meaningful shift in Manhattan luxury momentum.

The third signal is inventory.

New listings remain lower year over year, and luxury new-development supply is limited. That matters because when buyers have fewer compelling choices, the best-positioned resale properties become more valuable.

This week’s diagnosis is clear:

Demand is not disappearing.

It is concentrating around quality, scarcity, and strategic positioning.

Seller Advice

Sellers should be encouraged, but not complacent.

The Climate Index is favoring sellers, inventory remains constrained, and the $10M+ market showed notable strength. These are positive signals.

However, this remains a selective market. Buyers are active, but they are disciplined. They are not rewarding every listing equally.

For sellers, the opportunity lies in entering the market with precision: the right price, the right presentation, the right narrative, and the right competitive strategy.

This is especially important now if the spring market is extending into July. Sellers who are ready, realistic, and well-positioned may still benefit from active buyer demand before the deeper summer slowdown begins.

The strongest sellers are not simply putting their properties on the market.

They are diagnosing the market before the market diagnoses them.

Buyer Advice

Buyers should not assume that summer automatically means less competition.

If spring momentum extends into July, the best properties may continue to attract serious attention. Shrinking inventory and limited new-development supply mean that exceptional listings may become harder to replace.

That does not mean buyers should overpay. It means they should be prepared.

The best buyers in this market are identifying value early, understanding replacement cost, comparing inventory carefully, and moving decisively when the right property appears.

There is still negotiability in the market, especially for listings that have lingered or need repositioning. But buyers waiting for a broad summer slowdown may find that the most compelling properties are no longer available.

The best opportunity may not be the biggest discount.

It may be the property that others have not fully recognized yet.

Final Thoughts

The Manhattan luxury market is sending a more constructive signal than many expected at this point in June.

The spring market may have arrived late, but it may also last longer.

With $4M+ pending sales exceeding 2021 levels and only 2015 higher, this is a market worth watching closely. One week does not define a trend, but the direction of the data is meaningful.

For sellers, the opportunity is real — but strategy matters.

For buyers, timing, preparation, and selectivity remain critical.

The data tells us what happened.

The diagnosis reveals what to do next.

If you are considering selling, evaluating your property’s current market position, or trying to understand how today’s luxury market affects your next move, I would be pleased to share a private, customized perspective.

If you found this edition of the Pulse valuable, please consider sharing it with a friend, colleague, client or advisor who follows Manhahattan luxury real estate

Warm regards,

Carol

Carol Staab

Top 100 Sotheby's Global Real Estate Sales Advisor

Top 10 for Sotheby's Individuals Manhattan

My Recent Notable Sale Ritz Carlton $28.4M

Sotheby's International Realty.

Email: [email protected]

Cell: 917-273-7787

"The Pulse: Where data becomes insight. And insight drives results."

Website: CarolStaab.Com

Subscribe to the Pulse Here

|