The Pulse - Manhattan Luxury Market 5/14/25

Pulse

Pulse

Manhattan $4M+ Contracts Dip 10%, But Momentum Holds | Upper East Side Co-ops Strong Activity

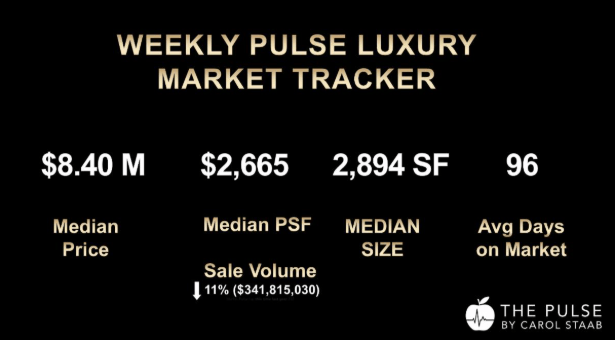

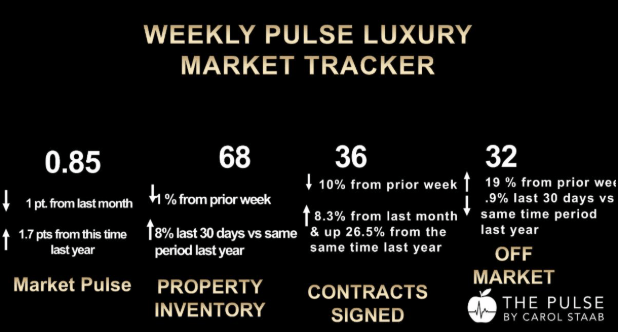

Deal activity last week remained notably above trend, with 36 contracts signed—a 10% weekly dip, yet still 80% above the benchmark of 20 contracts that defines a healthy $4M+ market.

Despite the slight pullback, buyer activity is strong. Signed contracts are up 8% from April and 26.5% year-over-year. Total sales volume rose 11%, showing that buyers are engaging—for properties priced correctly to the market.

The weekly numbers reflect healthy momentum, though signs of selectivity are increasing:

Buyer demand was concentrated in prime locations, with the Upper East Side leading the week:

Condos remained the majority of market activity, but co-ops had a standout week:

Negotiability remains modest. Most deals are still happening close to ask:

#1 – Madison House, PH60A

$25M | 5,151 SF | $4,855 PPSF | 1,298 DOM

After nearly four years, the seller and market aligned—demonstrating the long game sometimes pays.

#2 – 995 Fifth Avenue, Stanhope Condop

$24.25M | Originally $29.5M (2021)

This land-leased condop ultimately closed at a 17.8% discount—showing how smart repositioning creates opportunity.

National economic signals remain encouraging:

These developments suggest potential stability ahead—but Manhattan continues to move on its own terms.

Manhattan, however, remains asymmetrical to broader trends:

Prices rose just 2% post-COVID, and with 65% of luxury buyers paying in cash, mortgage rates have limited impact. Fundamentals—not speculation—are driving activity.

For Sellers:

Spring momentum is still in motion, but mid-June typically marks a seasonal slowdown. If your property isn’t seeing activity, the market is sending a message. Pricing and presentation need to reflect today—not a prior cycle. Many sellers wait too long to adjust—those who act now are getting ahead of the curve.

For Buyers:

Large discounts discounts remain a rarity. If you are looking for a deal, track the number of reductions and days on market. The best values often emerge right before summer and during July & August. For well priced renovated properties in prime locations be prepared to move quickly—those ready to act are in the strongest position.

If you'd like a custom report for your building, portfolio, or listing strategy, I’m happy to provide one or to answer any of your real estate questions. Email me here. Email me here.

Carol Staab has an innovative luxury real estate practice that provides an elite level of concierge service through unparalleled world-class marketing and a hands-on business approach. Her mission is to give her clients an exceptional experience while helping them achieve the best results possible.