The Pulse - Manhattan Luxury Market 6/3/25

Pulse

Pulse

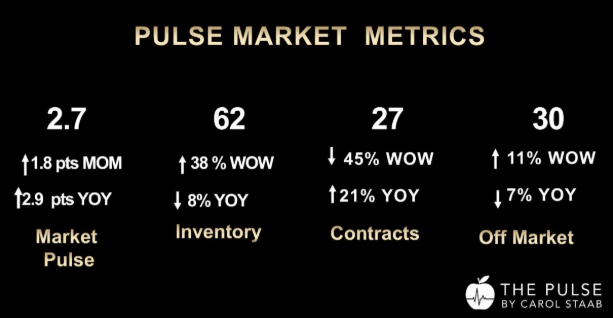

Manhattan $4M+ Contracts Dip 45% After Holiday—But Market Remains 35% Above Health Threshold

Following last week's surge—the strongest since fall 2021—the Manhattan luxury market took a natural step back. Contract activity over $4M fell 45% due to the Memorial Day weekend, a typical seasonal lull. Still, the underlying strength remains. The weekly total is 35% above the threshold for a healthy luxury market.

With 151 contracts signed in the last 30 days, activity is up 21% from the same period last year. We remain firmly in a high-functioning market, and as June begins, momentum is likely to return.

A post-holiday pause in contracts coincided with a noticeable increase in new listings—suggesting sellers are gearing up for a critical June window before summer quiets the market.

This week, Midtown outperformed all other areas—a shift from Downtown’s usual dominance. Upper East Side co-ops also contributed meaningfully to the week’s activity, as buyers sought value in prime locations.

Co-ops continued to show strength, particularly in the Upper East and Upper West Side, where long-term value, space, and location remain the driving forces behind buyer decisions.

New developments continue to attract discerning buyers—especially when architectural pedigree and brand strength align. A standout this week was The Henry, Naftali’s new Robert A.M. Stern-designed condo on West 84th Street. Residence 9A went into contract at $12.45M, a testament to the power of timeless design, meticulous detailing, and Upper West Side charm.

Nearly half of all buyers negotiated discounts, with a median reduction of 9%. Pricing precision is essential—this is not a market forgiving of overly aspirational asks.

A Market Pulse of 2.7 signals strong buyer demand relative to inventory. The Climate Index, though slightly down month-over-month, is still well above the 1.25 “easy seller” threshold—underscoring seller leverage in properly positioned listings.

The ultra-luxury tier continues to show resilience. Although the market pulse is just below last year’s level, demand remains consistent for turnkey, well-branded trophy properties priced to reflect current realities.

In the Hamptons, rental activity is down 30% from historical norms, with high-end rental discounts reaching 50–75%. Brokers attribute the pause to concerns over potential tariffs. However, sales remain strong, as buyers see long-term value in the region.

In Manhattan, luxury rental inventory rose for the first time in three months, as some would-be sellers shifted to renting. Meanwhile, discounts in the luxury rental segment hit a record low, and the median rent remains flat year-over-year.

Inflation is holding at 2.3%, just above the Fed’s 2% target.

Mortgage rates remain around 6.9%.

President Trump met with Fed Chair Jerome Powell to advocate for a rate cut, but Powell reiterated that future action will depend entirely on the data.

Market indicators are on your side—but timing is critical. With market pulse and seller climate both up year-over-year, June is your prime window to transact before activity slows. But 44% of deals involved discounts last week—buyers are pushing back when value isn’t clear.

If your home has stalled and you're unwilling to adjust the price, consider renting (especially if it's a condo or townhouse), or taking it off-market and relaunching in September with refined presentation and strategy.

Sellers are motivated to act before summer travel takes hold. Now is your chance to negotiate intelligently, especially on listings with 100+ days on market. Co-ops in top neighborhoods continue to offer real value.

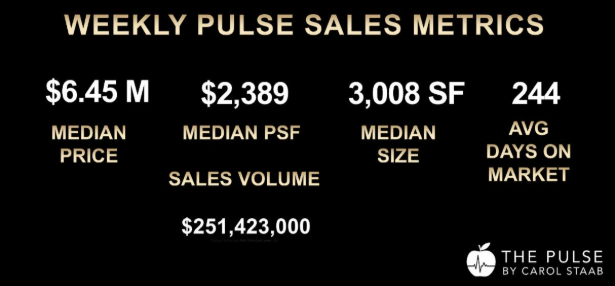

#1 – 988 Fifth Avenue, #4

Resale Condo | Upper East Side

$20M (↓ $2M from original ask) | 822 Days on Market

3 Beds | 5.5 Baths

An elegant prewar residence with commanding Fifth Avenue views. After nearly two and a half years on market, it finally found its buyer—a clear example of pricing strategy meeting market reality.

#2 – 211 West 84th Street, The Henry #9A

New Development Condo | Upper West Side

$12.45M | 3,726 SF | $3,800 PPSF | 5 Beds | 5.5 Baths | 103 Days on Market

A marquee contract at The Henry, Naftali Group’s newest Upper West Side triumph designed by Robert A.M. Stern. This residence delivered expansive living, timeless architecture, and luxurious detailing—securing $3,800 per square foot and reinforcing buyer appetite for design-driven new development in prime locations.

A 45% week-over-week drop might seem dramatic—but zoom out, and it’s clear: we’re still operating well above historical benchmarks. The dip was seasonal, not structural.

We are now entering the final stretch before the summer slowdown, when buyer attention and deal flow tend to soften. June presents a narrow but meaningful window for both sellers and buyers to make strategic moves. Whether your goal is to exit or enter the market, timing and execution are everything.

For a custom report on your property, building, or neighborhood—or to explore how this week’s insights apply to your goals—reach out directly.

Thank you for your loyal readership of the Pulse. Be sure to share it with others who may find it of value.

Carol Staab has an innovative luxury real estate practice that provides an elite level of concierge service through unparalleled world-class marketing and a hands-on business approach. Her mission is to give her clients an exceptional experience while helping them achieve the best results possible.