Hi Carol,

The final week of August saw 17 contracts signed at $4M and above—down 23% from the prior week. For the month, 88 contracts were signed, exactly the same as August 2024, underscoring the Manhattan luxury market’s resilience even in its slowest seasonal stretch.

But the defining story of 2025 remains intact: new inventory is consistently down. August brought just 72 new listings, 23% fewer than last year. Throughout 2025, fewer sellers have been willing to bring fresh product to market, keeping supply lean. At the same time, off-market withdrawals fell 27% YoY, meaning more sellers are staying the course instead of retreating.

Market Snapshot

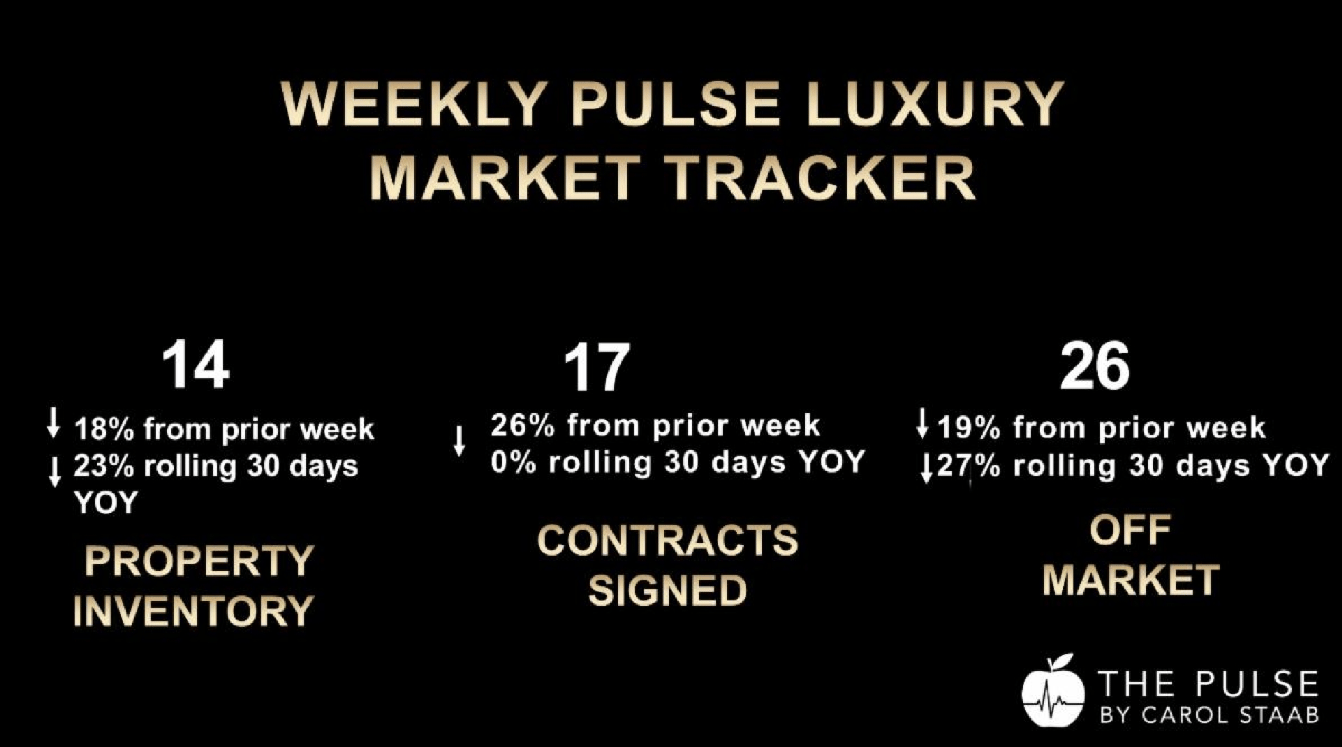

- Contracts Signed: 17 (↓ 23% WoW; 88 in August, fat YoY)

- New Listings: 14 (↓ 18% WoW; 72 in August, ↓ 23% YoY – continuing 2025’s lean inventory trend)

- Overall Inventory: ↓ 23% YoY

- Off-Market Listings: 26 (↓ 19% WoW; 123 in August, ↓ 27% YoY – more sellers staying active)

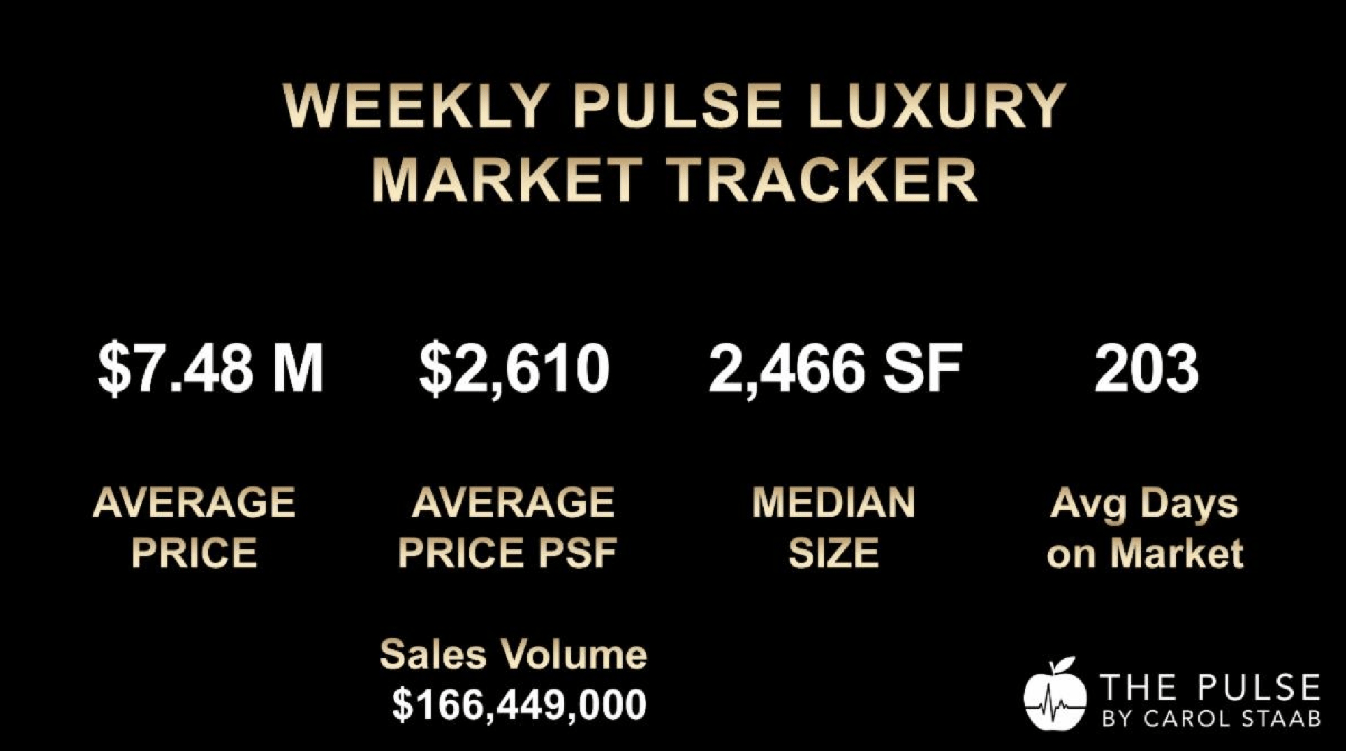

- Sales Volume: $127,240,000 (↓ 24% WoW)

- New Development: 2 contracts, 12% market share

- Discounts: 10 contracts (59%) with reductions; median discount: 6.5%

- $10M+ Segment: 4 contracts, 24% market share (a strong performance)

Market Indicators

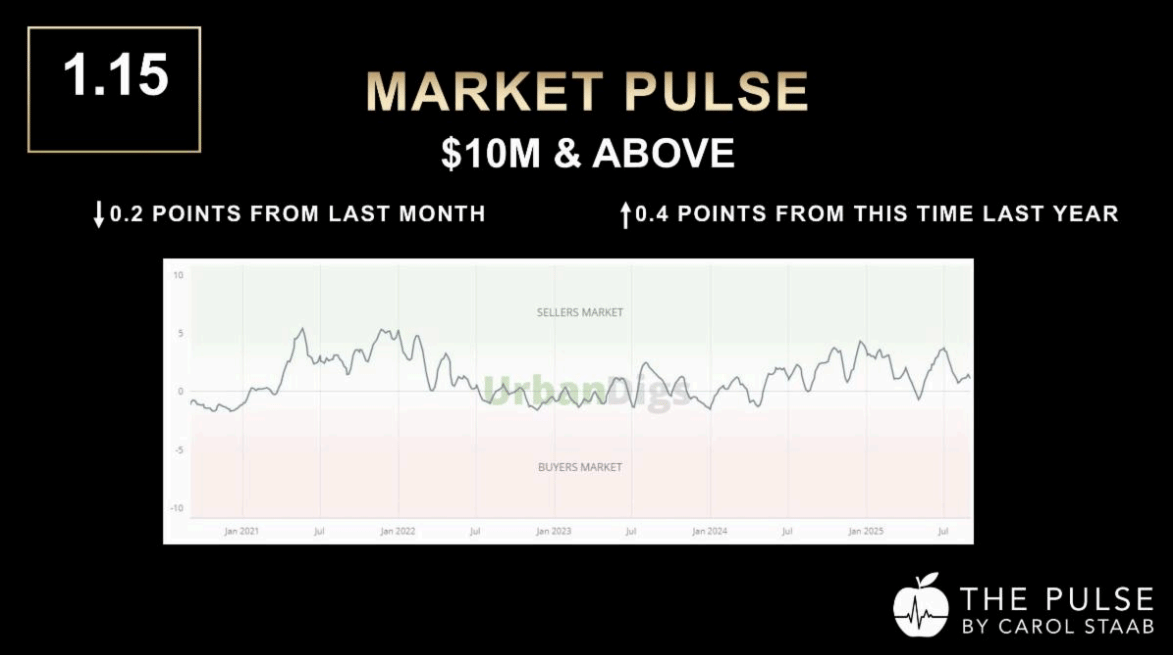

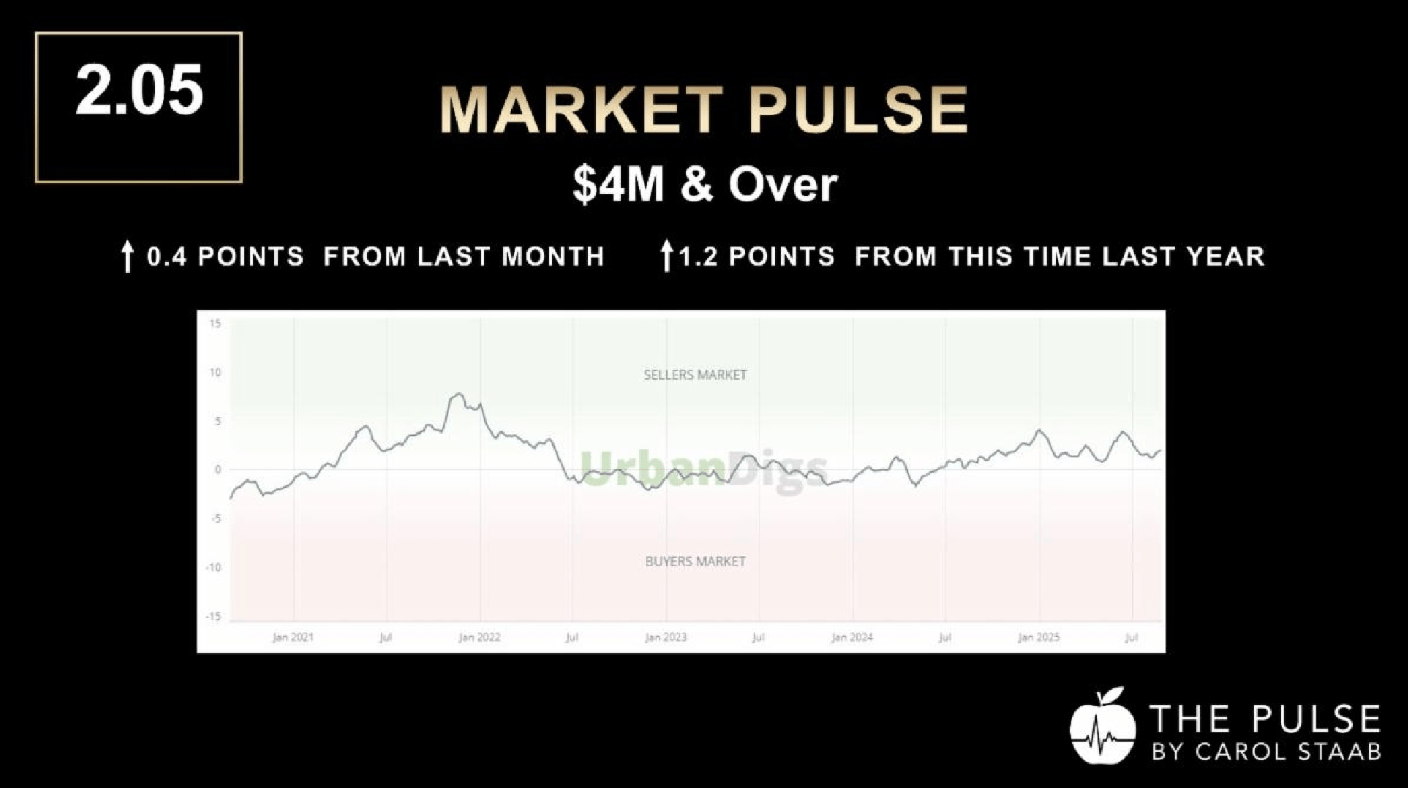

Market Pulse -Ratio of Supply & Demand

“Positive = stronger than seasonal norms; negative = weaker.”

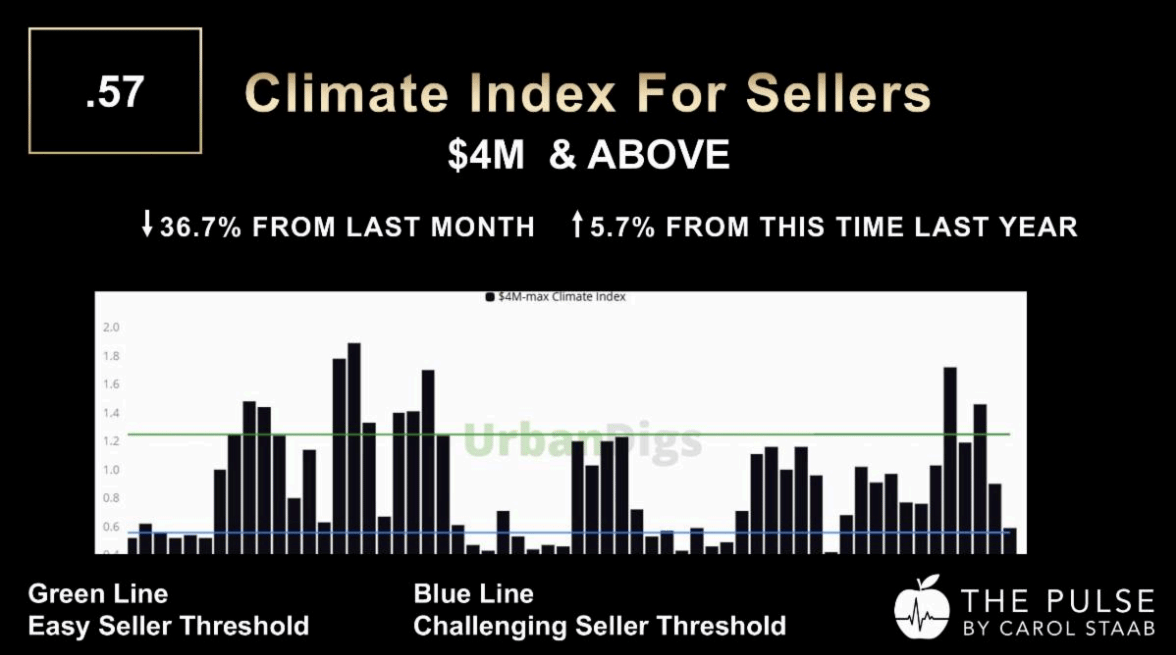

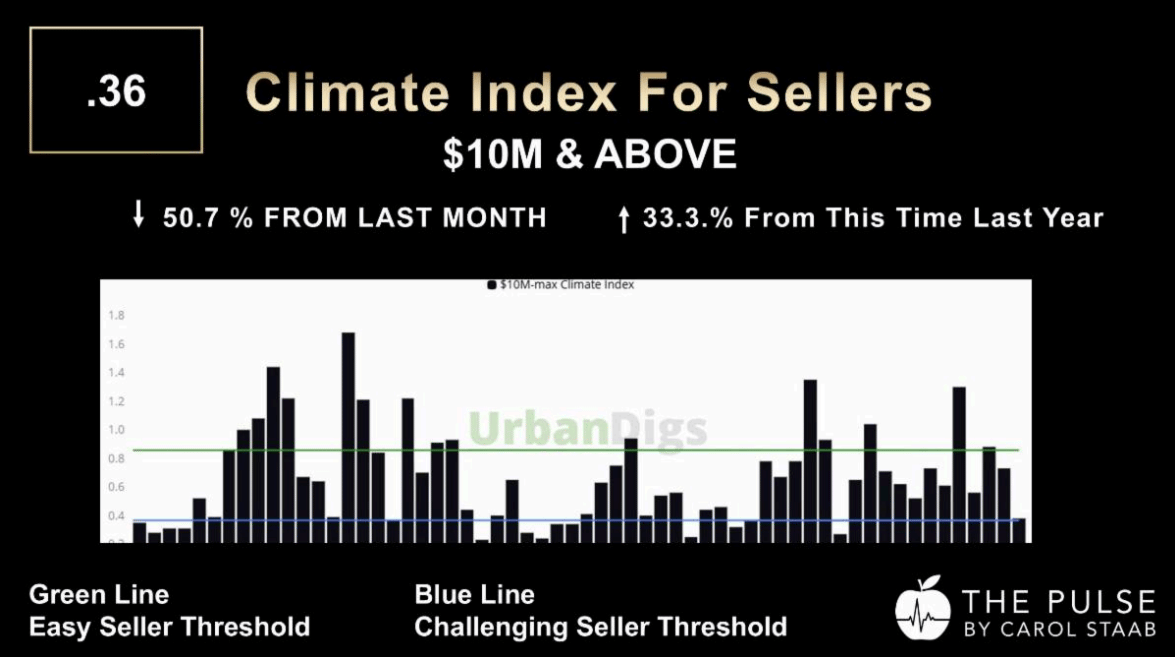

Climate Index - tracks signed contracts against off market listings to gauge seller market condition. A higher index favors sellers.

- Market Pulse $4M+: 2.05 (↑ 0.4 MoM; ↑ 1.2 YoY)

- Climate Index $4M+: 0.57 (↓ 36.7% MoM; ↑ 5.7% YoY)

- Market Pulse $10M+: 1.15 (↓ 0.12 MoM; ↑ 0.4 YoY)

- Climate Index $10M+: 0.36 (↓ 50.7% MoM; ↑ 33.3% YoY)

Neighborhood & Property Type Performance

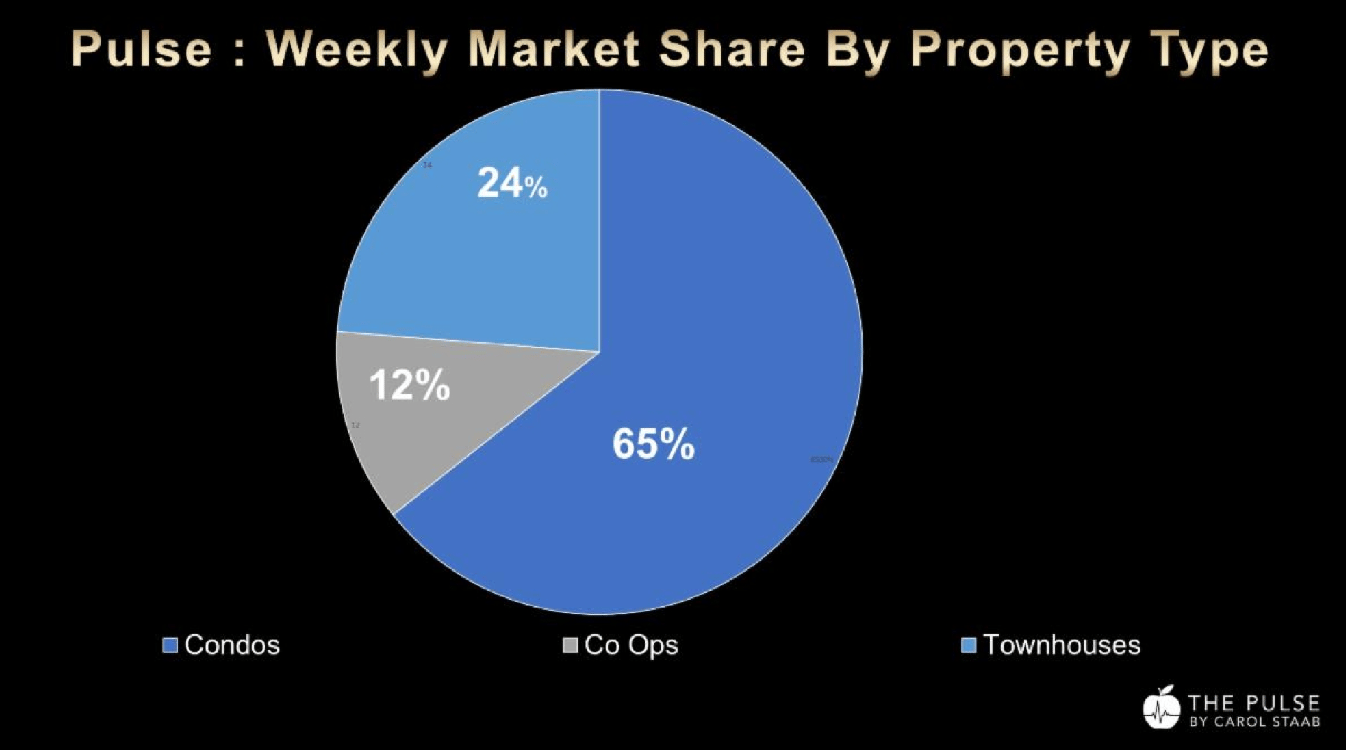

- Condos: 11 contracts, 65% share

- Co-ops: 5 contracts, 29% share

- Townhouses: 1 contract

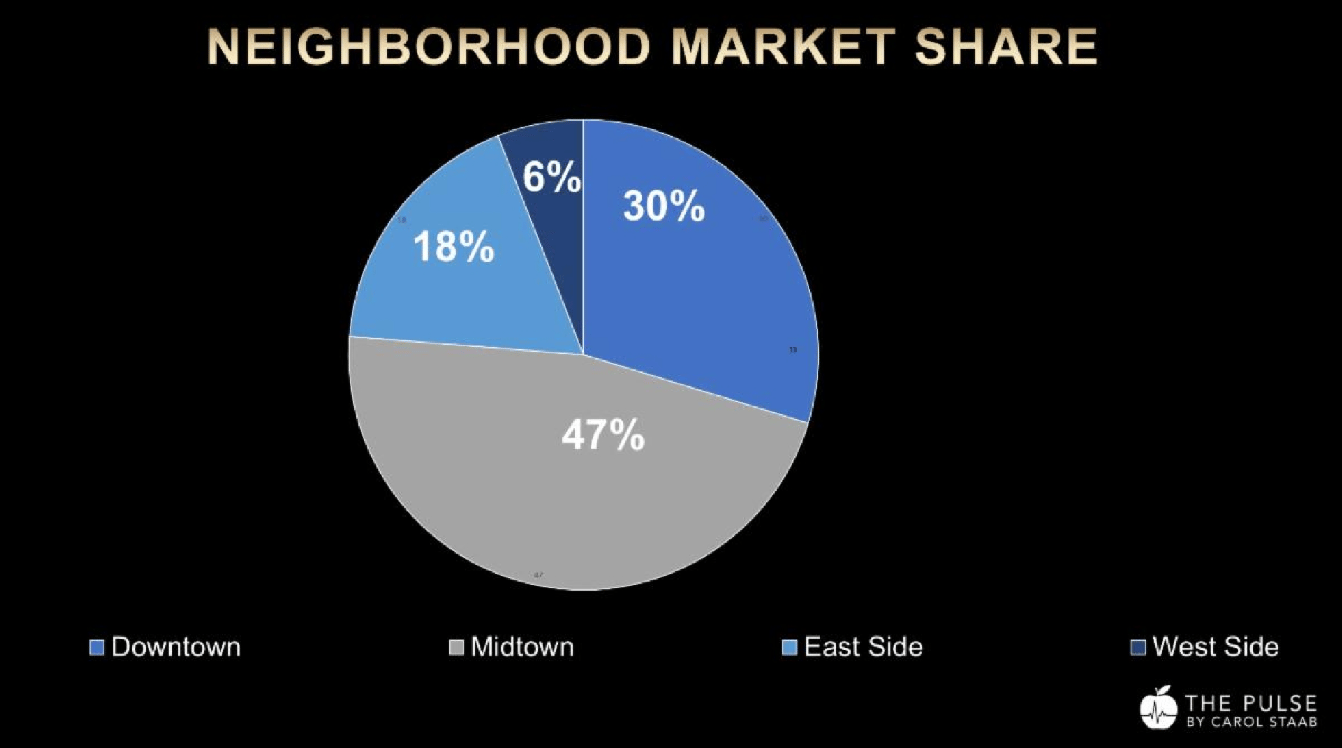

- Midtown: 8 contracts, 47% share (leading the market)

- Downtown: 5 contracts, 30% share

- Uptown: 4 contracts, steady co-op activity

Top 2 Contracts – See All 17 Contracts

#1 – 49 East 80th Street Townhouse – asking $15.9M (reduced $975,000) Upper East Side townhouse | 8 bedrooms, 5.5 baths | 9,193 sq. ft. | $1,729 psf -371 days on market.

#2 – The Highline - 500 West 18th Street, #24D – asking $14.53M

Chelsea new development condo | 4 bedrooms, 4.5 baths | 4,951 sq. ft. | $3,677 psf

Insights & Advice

For Sellers

- Lean Supply Advantage: With new listings down 23% YoY, serious sellers face less competition entering the market.

- Be Prepared for Mid-September: Fresh supply traditionally arrives after Labor Day. The key question is whether new listings will rebound — or remain weak, as they have throughout 2025. Either way, re-examine your positioning and pricing now to ensure you stand out.

- Presentation is Perception: Precision pricing and fawless presentation remain your edge in the luxury segment.

For Buyers

- More Choice Ahead — But How Much?: September usually brings more listings, but 2025 has consistently delivered fewer new options. Don’t expect abundance.

- Discounts in Play: 59% of contracts last week closed with discounts, median 6.5%. Long-market properties remain negotiable, but unique, well-priced homes are still competitive.

- Act Decisively: When the right property appears, hesitation can mean losing out.

Macro Context

- Economy: Consumer spending rose in July at the fastest pace in four months, showing resilience despite ongoing tariff pressures. The job market remains sluggish.

- Rates: The Fed is expected to cut rates by 25 basis points in September. If mortgage rates ease, buying power will improve, potentially fueling competition.

- Local Dynamics: While headlines speculate about buyer pullback, luxury contracts continue to hold steady, matching last year’s performance.

Final Word

August ended with 17 contracts in the final week and 88 overall—matching last year’s pace. The defining theme of 2025 remains intact: new inventory is consistently down 23% YoY, while more sellers are staying active on the market. As we enter the fall, the question is whether September’s fresh listings will break this year’s weaker trend—or reinforce it.

For sellers: Precise pricing and standout presentation are critical before the mid-September rise in listings.

For buyers: Lean supply means that when value appears, hesitation can be costly.

Thanks for reading The Pulse. If you find this of value, please share it with others who follow Manhattan’s luxury market.

Would you like to know how today’s market positioning affects your property?

I’d be glad to prepare a tailored report specifc to your home or building.

Warm regards,

Carol

Carol Staab

Global Real Estate Advisor

Sotheby's International Realty.

650 Madison Avenue

The Pulse: Where data becomes insight. And insight drives results.

Subscribe to the Pulse

HERE